A couple weeks ago I talked about the market either broadening out (our preferred outcome) or eventually the market falling in on itself.

The reason was that the market cannot continue to go up with only seven stocks keeping things elevated. Eventually either the big stocks stop working (and everything goes down) or the rally broadens out and the rest of the market plays catch up. Since the CPI data last week, we have seen a massive rotation toward the rest of the 493 S&P 500 companies, the Russell 2000, and mid-cap stocks. We’ve even seen international stocks and bonds outperform.

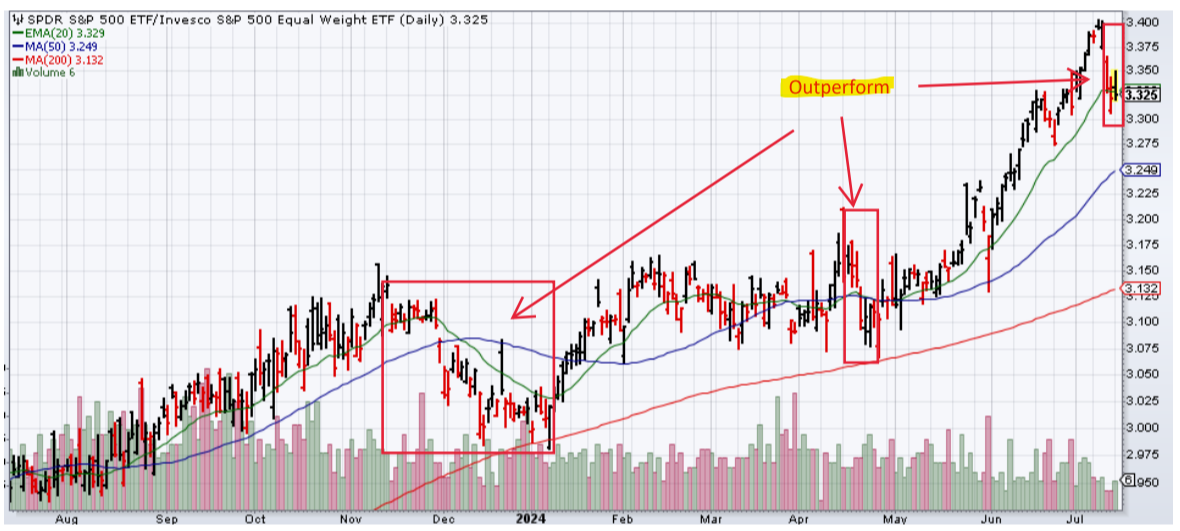

That’s the outcome we would like to see. Let’s take a look at the charts. Here is a chart comparing S&P 500 market cap weight versus equal weight.

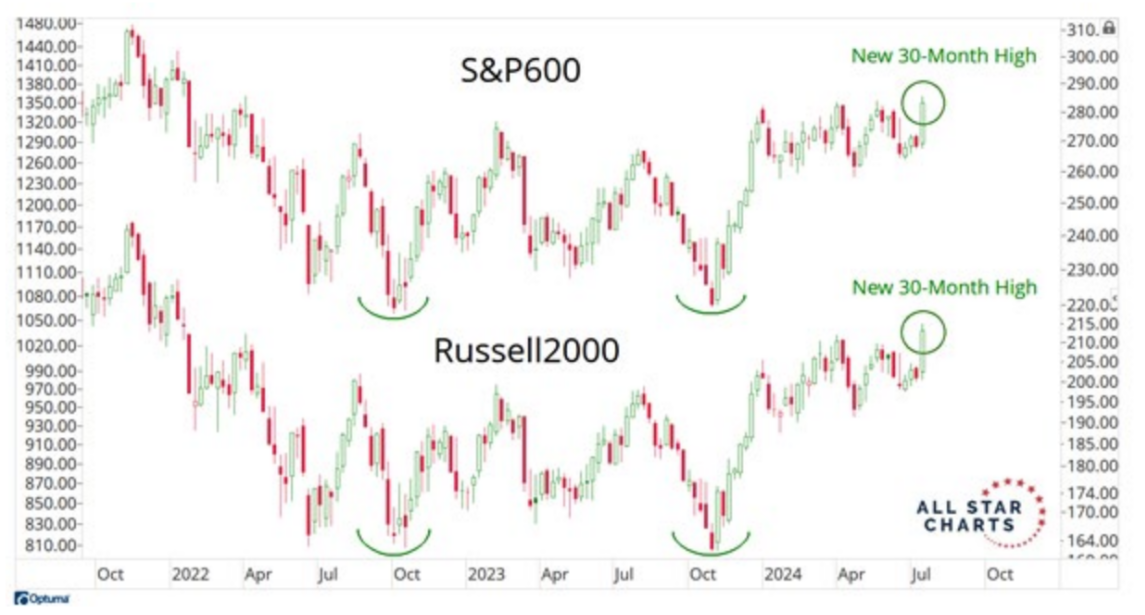

Here’s the S&P 500 versus the Russell 2000

When the chart goes down, that shows the Russell 2000 outperforming. Likewise, when the chart is moving upward, the S&P 500 is outperforming.

Here’s another chart of two different small cap indexes. They are breaking out to new 30-month highs!

In fact, most equal-weighted sectors are now starting to beat their market-weight brethren. Below is the chart of the discretionary sector – market cap weighted vs. equal weighted.

After interest rates moved back up from roughly 3.8% on the 10-year treasury (topping out at almost 4.75% in April), the 10-year treasury has moved back down to 4.25% (middle of the range).

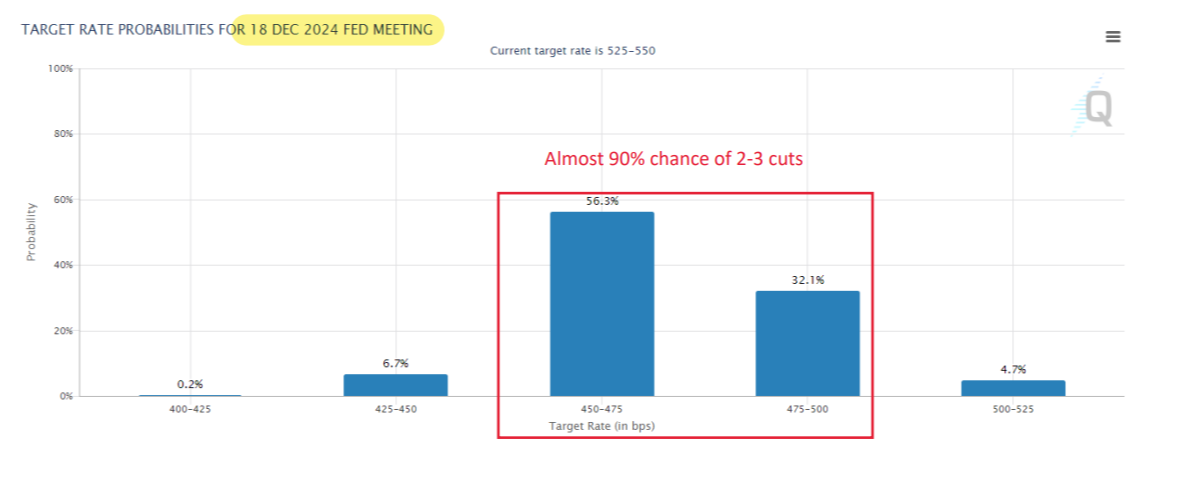

The probabilities of rate cuts by the Federal Reserve by the end of the year are looking at 50-75 basis point worth of cuts. A month ago, the odds were for only one 25 basis point cut by year end.

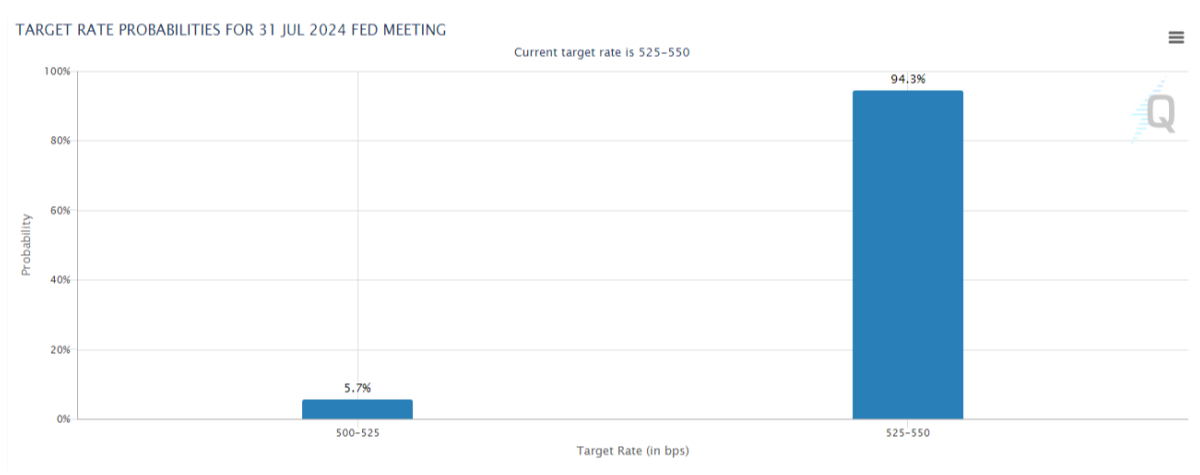

The big question is whether the FED is behind the curve AGAIN or are they playing this correctly? I think they are a little behind the curve but that a cut in July would get them caught up. The market is not expecting them to cut rates this month, as seen in this next chart.

We will be getting housing starts this week, as well as numbers on unemployment claims. If these numbers continue to be weak, that may make the FED act a little sooner than they would prefer. At a minimum, there doesn’t seem to be any reason to talk about RAISING interest rates for the time being.

We would like to pass along our condolences to those injured or killed at the Trump rally over the weekend. Violence should never be the answer to disagreements (political or otherwise).

I hope you have a good week. Reach out if you have any questions! Oh, and expect a couple of financial planning focused pieces over the next couple of weeks, as my editor/publisher Andrew is on baby watch right now (baby boy due in the coming days) and likely won’t be able to assist for a bit. He’s going to tee up some (hopefully) timeless planning advice to publish in his absence.