Happy New Year! I hope you all had a wonderful holiday season. Between being sick for part of that time, the holidays themselves, and the holidays being on a Wednesday, it seemed more difficult to do my regular Monday piece. But hey, we’re back at it in the New Year. We’ll start with a market commentary, and next week we’ll hit you with some planning updates focused on things that have changed with the turn of the calendar (e.g. contribution limit changes). If an RMD is in the cards for you this year, we’ll be in touch individually about what that amount will be and how you wish to tackle it.

Speaking of the calendar, we were on track to have a normal week this week and then we found out that the markets will be closed on Thursday in honor of Jimmy Carter’s passing. May he rest in peace and may we all pause to recognize his service to our nation and the world as a whole.

In addition to that, most of the United States east of the Rockies will be in for the dreaded Polar Vortex. For those of you on that side of the country (and not in Florida!), please be careful out there!

Speaking of polar, how about this news from our friends in the Great White North. After the incoming President teased about Canada becoming the 51st state, Justin Trudeau is stepping down. No, the jokes were not the cause. Pressure has been building for quite some time. The state of the economy in Canada is weak at best. Perhaps an isolated event, or an indicator of more sea change coming to global politics and markets in the year ahead. We shall see.

Zooming out and changing our focus, here are the major countries that are sub-50 for their PMIs. Keep in mind that sub-50 means the economy is in contraction. The US currently sits at 55.4 for our PMI, though some more focused measurements (such as manufacturing) are in contraction.

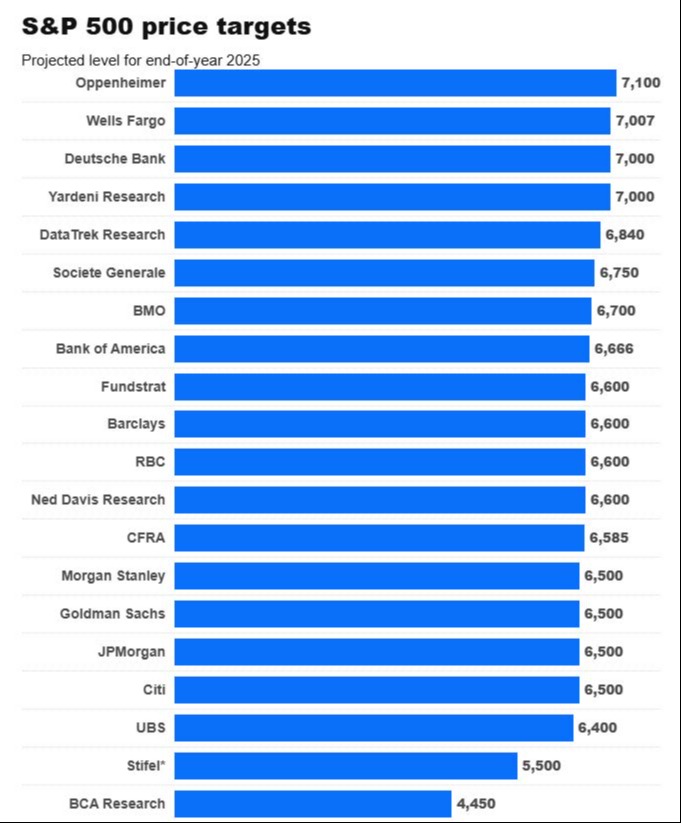

Meanwhile, most of the large financial companies have come out with their predictions for 2025. Keep in mind that most of them were off wildly for 2024. But like Yogi Berra said, “It’s hard to make predictions, especially of the future.” This time next year we will see how they did. For reference, the middle of the pack here represents about a 10% increase on the S&P 500 for the year.

After a couple of “hot” months of inflation numbers it seems that both the jobs numbers and inflation have settled in what we would call the goldilocks area. Remember that we thought the 2% number was a made up number on the way up from 2008 to 2020. Now, the FED has anchored itself around that number on the way down too. Inflation since the Great Depression has been between 3% and 3.25% and nothing bad really happened.

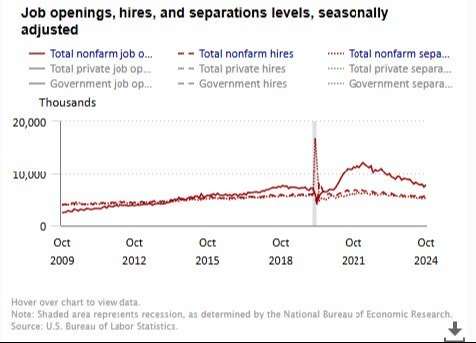

If the FED had said that’s what it was aiming for, we would be in good shape right now. Instead, we have an inflation rate that is “stubbornly” above the 2% rate (and not likely to head back there unless we get a recession). The unemployed versus JOLTS numbers are starting to come back in line.

Rather than a 2:1 margin, it is now less than 1.5:1. You can see from the chart above that after COVID the job market got crazy and there were many more job openings than job seekers. As an aside, we are still trying to figure out what happened to the 7 million (mostly working aged men) that disappeared from the job market since COVID.

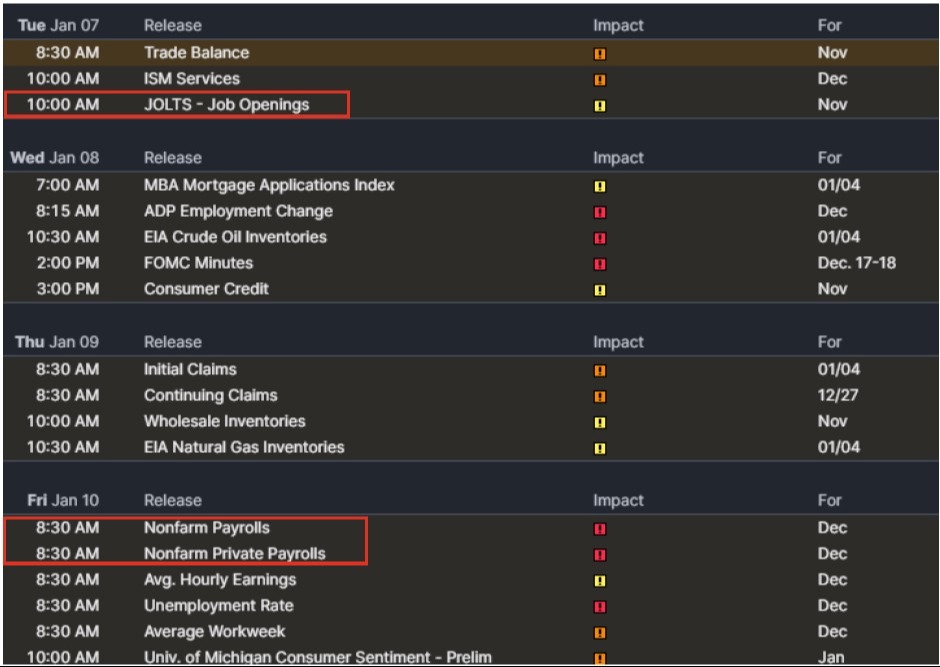

The JOLTS number comes out tomorrow while the weekly unemployment number comes out on Friday. So, we will see what that number looks like. Here are the economic reports coming this week.

Last but not least, Ford and General Motors had the highest annual sales since 2019. Electric vehicles were up 38% and 50% respectively, but that is coming off very low levels. Those electric trucks that I talked about over a year ago, I don’t think those will be matching expectations any time soon.

That’s it for this week. If you have any questions, please reach out and we will be happy to have a conversation.