It’s kind of funny, late Friday after the markets closed, Moody’s (one of the big 3 ratings agencies) cut the US debt from Aaa to Aa1. That is earth shattering news, right? Well, not so much.

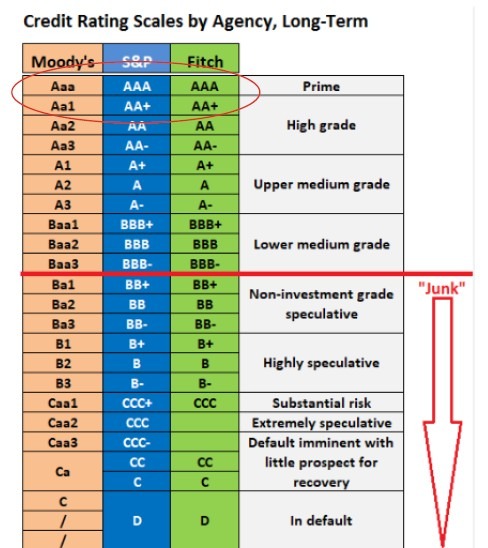

Here’s what the credit scales look like.

You can see that the US government debt was lowered a whole one (1) notch. From the best rating possible to the second highest rating. Oh my gosh, look out below.

What’s even worse?

The stock market is crashing. Ok, not really. While 30-year treasuries are now over, wait for it, 5% and 10-year treasuries are now back to 4.5% the world has officially come to an end. Well…not really.

The markets this morning are using the downgrade as an excuse to sell off.

Meanwhile our favorite market index is also down about a half percent.

But let’s put this in perspective. Moody’s is really just late to the party. What does that mean? Does anyone remember when Standard and Poors (S&P) lowered the debt rating of the US debt?

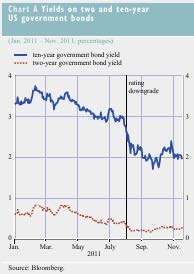

That’s when the party started. After that happened, the financial pundits said that was the end of the bond market and rates would go much higher. Here’s what happened.

They went down in yield.

Then the other ratings agency, Fitch, lowered their rating also from AAA to AA+ on…wait for it…

Almost 2 years earlier than Moody’s, but 12 years after the first downgrade from S&P. And what happened to interest rates? Don’t forget this was a couple years after the FED said inflation was “transitory,” and rates had already gone from below 1% to a little above 4%. The rates have gone up a little, but of little consequence from the debt downgrade. In fact, the 10-year treasury has basically bounced between 4% and 5% since then. Today we are exactly in the middle of that range.

So, this downgrade from Moody’s is sort of comical, in my opinion, coming a mere 14 years after S&P downgraded US debt. Here’s what they had to say about the downgrade:

Over more than a decade, US federal debt has risen sharply due to continuous fiscal deficits. During that time, federal spending has increased while tax cuts have reduced government revenues. As deficits and debt have grown, and interest rates have risen, interest payments on government debt have increased markedly.

Without adjustments to taxation and spending, we expect budget flexibility to remain limited, with mandatory spending, including interest expense, projected to rise to around 78% of total spending by 2035 from about 73% in 2024. If the 2017 Tax Cuts and Jobs Act is extended, which is our base case, it will add around $4 trillion to the federal fiscal primary (excluding interest payments) deficit over the next decade.

As a result, we expect federal deficits to widen, reaching nearly 9% of GDP by 2035, up from 6.4% in 2024, driven mainly by increased interest payments on debt, rising entitlement spending, and relatively low revenue generation. We anticipate that the federal debt burden will rise to about 134% of GDP by 2035, compared to 98% in 2024.

Despite high demand for US Treasury assets, higher Treasury yields since 2021 have contributed to a decline in debt affordability. Federal interest payments are likely to absorb around 30% of revenue by 2035, up from about 18% in 2024 and 9% in 2021. The US general government interest burden, which takes into account federal, state and local debt, absorbed 12% of revenue in 2024, compared to 1.6% for Aaa-rated sovereigns.

While we recognize the US' significant economic and financial strengths, we believe these no longer fully counterbalance the decline in fiscal metrics.

Wow, really? You finally got to the point where deficits matter and debt service matters? All I have to say is, “better late than never.” Meanwhile, nothing has really changed. We will still have large deficits, and our debt service will continue to climb. The argument could be…should the US be rated as high as it is?

You want to see some fireworks, watch what happens if that was ever to come into being.

As always, please let us know if you have any questions about this or any other topic. We will be happy to have a conversation.