Hot off the presses! The US leading economic indicators have just been released.

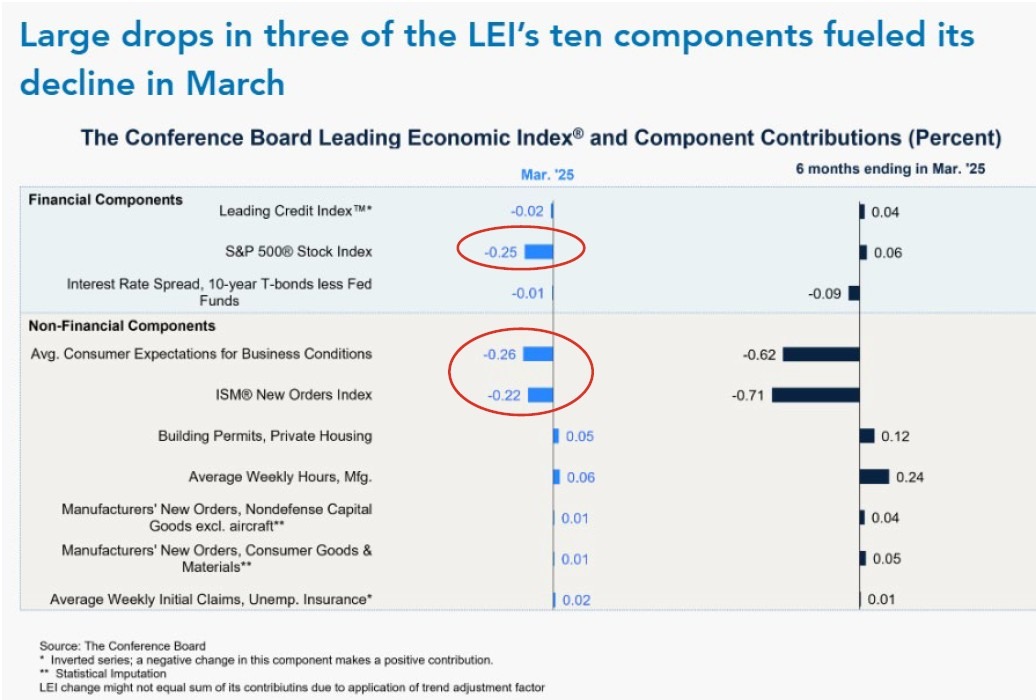

It’s not pretty. Now you have to take into account this is for the month of March, so already backward looking – but that number was -0.7%.

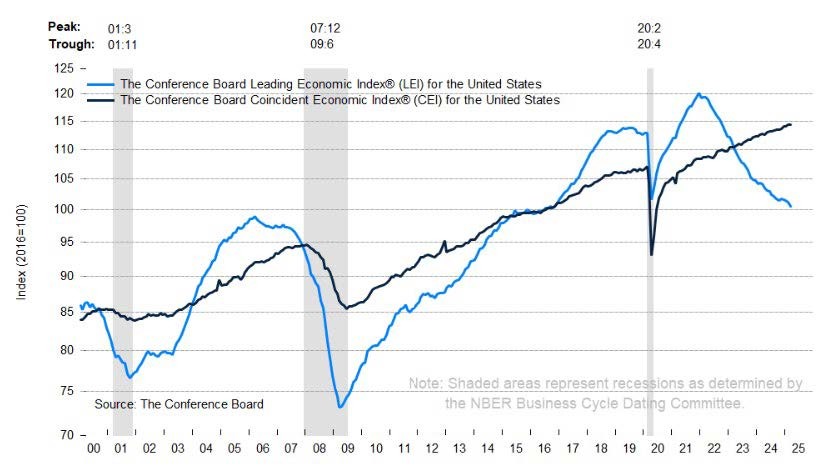

You can see that the US LEI have been going down since 2021 and this was the largest decline since September 2022. Broken down below, the LEI was pulled lower by three things. The stock market, consumer expectations, and the ISM new orders. Some of the other constituents are not always that important, but the three referenced above are probably the most important of all the constituents. They tend to be the most forward-looking of the group.

Shifting gears, in our view, it is important that many “independent” organizations of government remain independent. Not to get into too much of a political discussion, because that’s not what we’re here for, but the “firing” of the FED chair is not something that should be done.

Now, you know that I’m no huge fan of the Federal Reserve, and I think mostly they manage interest rates and monetary policy out of the rearview mirror. But that’s no reason to fire them. And yes, while it’s true that I think the FED is behind the curve AGAIN, I think that’s more a symptom of process and academics than willful negligence or mismanagement.

Much of them being behind the curve has to do with tariffs, taxes and jobs. None of these things in the short run are particularly helpful for the FED’s dual mandate of full employment and stable prices. While tariffs are generally counterproductive (from every country’s point of view), the way this administration has gone about implementing their tariffs has been particularly counterproductive (at least in the short term). Will there be “deals” coming through? Probably. But what damage will be done in the meantime? We’ll have to wait and see.

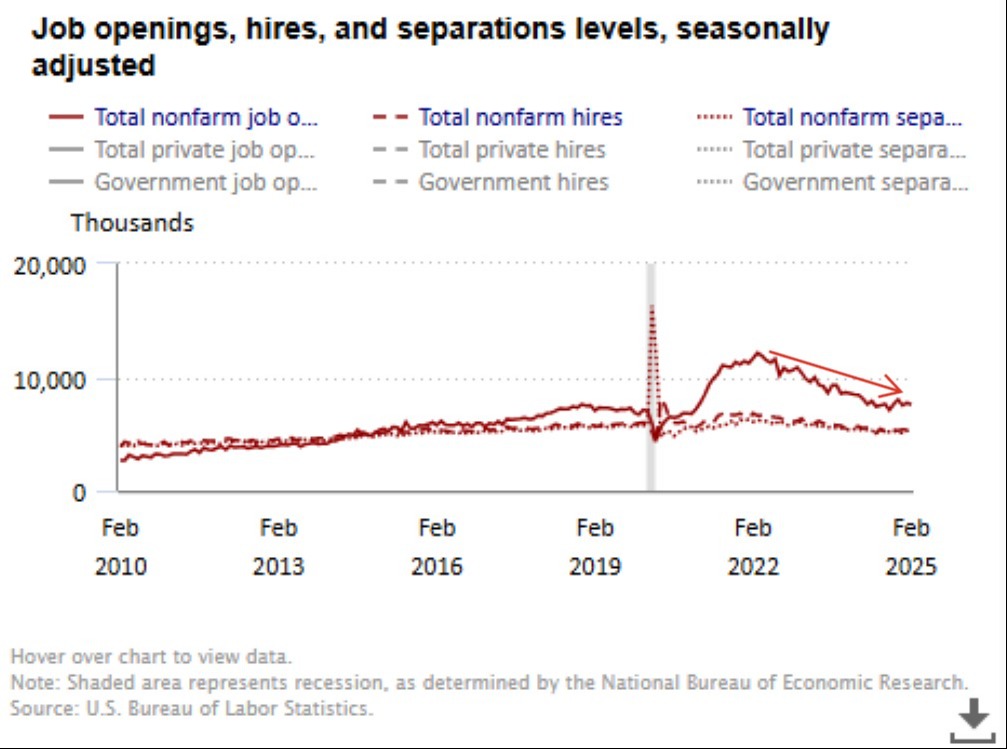

Jobs were becoming harder to get as we were going into 2025. You can see from the JOLTS report below, that job openings had come down from around 12 million to about 7.5 million in February.

We haven’t seen a huge spike in layoffs, nor have we seen a huge spike in the unemployment numbers. Partially that is because the US economy is in decent shape. Good enough to fit into the “soft landing” camp that I have been in.

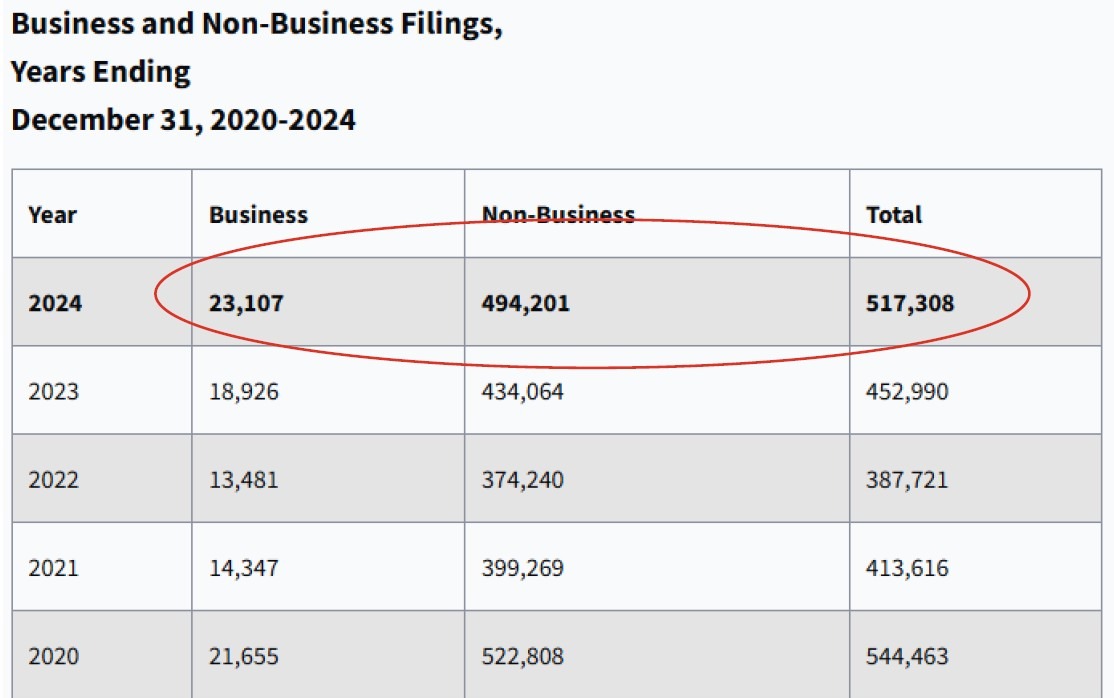

Now, that doesn't mean that something can’t “break,” and we have talked about many of those possibilities. Higher interest rates are certainly taking their toll on businesses. Business bankruptcies have risen by 14.2% through last year. Not only that, but non-business (personal) bankruptcies have increased to the most since COVID.

As part of the many corporations declaring bankruptcies, there have been many trucking companies that have gone bankrupt over the last 3 years.

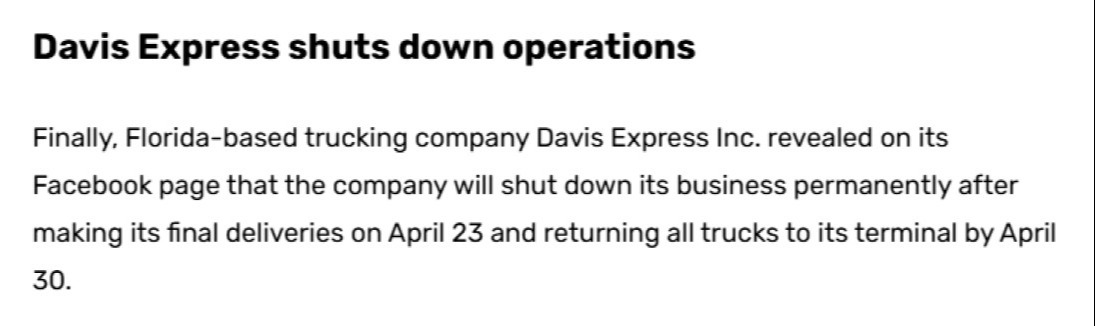

Apparently, it’s bad enough that some are closing without even declaring bankruptcy. Case in point – Davis Express of Florida.

I don’t know much about the trucking industry, but I think those are pretty well-paying jobs and Davis Express is laying off 140 drivers and will keep mechanics around until they can sell their trucks and assets.

Some of this is necessary, although not easy. The trucking industry may be a bit of an outlier, but interest rates staying high (potentially higher depending on tariffs and inflation) could put a lot more companies in vulnerable situations. This, of course, may in turn put individuals in vulnerable situations.

Wrapping it up, from LEI readings to trucking company anecdotes, risks of a recession remain elevated. As long as they do, markets will likely remain choppy. After all, bear markets that are paired with recessions are typically significantly more painful than non-recessionary bear markets. As such, investors will continue to keep an eye on things, searching for some clarity in the midst of great uncertainty.

If the current clouds of uncertainly have you losing sleep or there are questions you’d like to ask, please reach out and we will be happy to have a conversation.