The “One Big Beautiful Bill” (OBBB) is no longer news. Its passage is well understood, though support for it certainly varies. What is common though is that the impact of the bill on individual circumstances remains murky for most. To help provide some clarity, we’re going to highlight here a couple of key provisions that are broadly impactful, with brief mention to a couple of others that are more marginal in their reach.

The most impactful measure of all is one you may not even notice, as it doesn’t really change anything. It is that the individual income tax rates that have applied for the past few years are now made permanent. In and of themselves, these rates mean lower taxes for everyone compared with allowing rates to revert to pre-TJCA (Tax Cuts and Jobs Act of 2017) rates – though other provisions that were passed in the OBBB may result in higher or lower taxes for many.

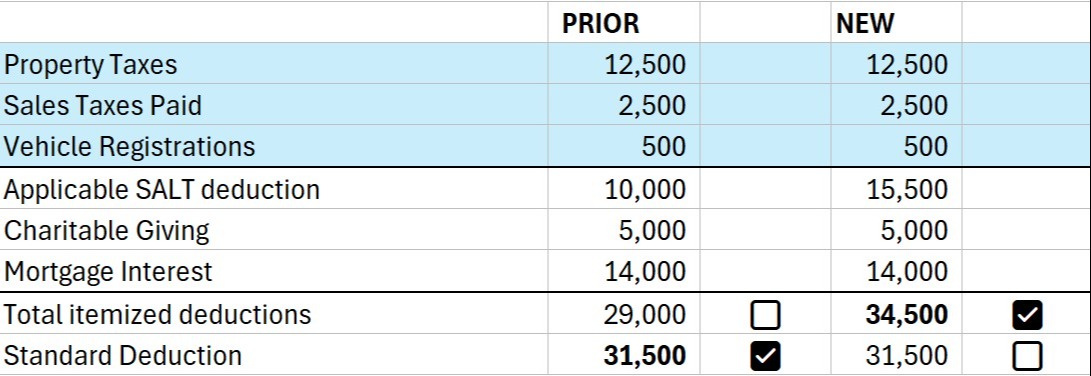

So, what are some of these other provisions. Let’s start with the new SALT (state and local tax) deduction cap. Since the TJCA was passed in 2017, deductions for these taxes were capped at $10,000 per year (with no adjustments for inflation) (there was no cap in years prior to 2017). For those that continued to itemize their deductions, this often meant lower deductions than would have otherwise been enjoyed. For example, if your property taxes were $15,000 and your other local taxes were $3,000, you were unable to deduct $8,000 of these expenses. In reality, this cap helped push many taxpayers to use to the standard deduction, as it was harder to eclipse the standard deduction amount with itemized deductions when this cap applied (especially for those with no mortgage interest). This is all about to change, though. Starting this year, the cap has been increased to $40,000 (increasing 1% annually through 2029, after which the entire cap reverts to $10,000). Note, however, that the maximum deduction begins phasing down once income reaches $500,000 (filing single or married/jointly). Let’s look quickly at an example. In this example, a married couple is earning $300,000, owns a home with a mortgage, and is charitably inclined. How does their deduction change with the new law?

In our example here, this couple would have elected the standard deduction under prior law (note, the standard deduction also received a small bump up for 2025, increasing from the previously planned $30,000 for joint filers to $31,500. For single filers, it was increased from $15,000 to $15,750). With the new SALT cap, they will now elect to itemize their deductions and will receive an additional $3,000 of deductions without any changes to their expenses. Assuming a 24% marginal tax bracket, this translates to a $720 annual tax savings at the federal level.

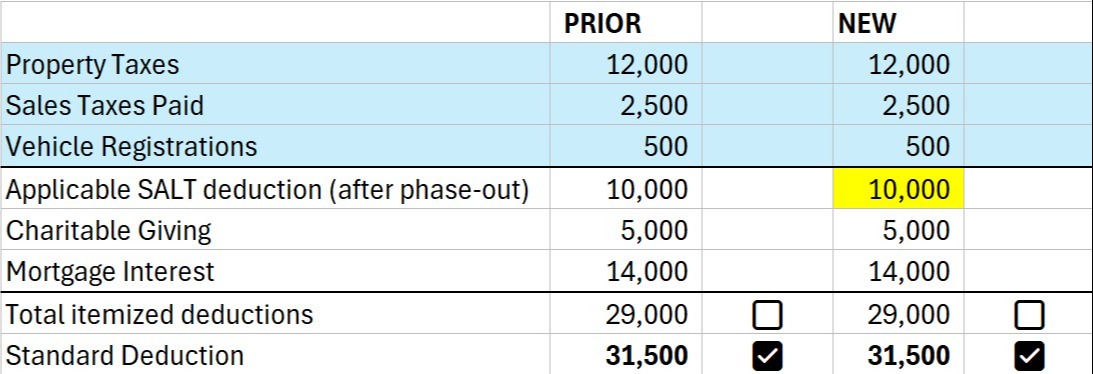

But what if this couple instead earned $600,000? How would things work then? We’ll spare you the details on how the aforementioned phase-out is calculated, and instead just show you its impact. As you’ll see, they end up right back where they started, as the phase-out reduces their SALT deduction to the original $10,000 limit.

Moving on, let’s look at another key change to deductions. This one applies if you are age 65 or older. In tax years 2025-2028, a $6,000 deduction is added for each taxpayer ($12,000 for a couple filing jointly). This is in addition to the $1,600 bonus standard deduction already received by each individual if age 65+ ($2,000 if filing single). The kicker here is that this $6,000 bonus phases out for modified adjusted gross income (MAGI) above $150,000 for joint filers, fully phasing out at $250,000.

Let’s assume you are a couple (both age 65+) that does fully qualify by way of having a MAGI <$150k. For 2025, your standard deduction just increased from $33,200 to $45,200. This would result in tax savings of up to $2,640 per year at the federal level.

Before we continue, let’s point out a potentially beneficial planning technique that results from this 65+ deduction change. Because this deduction is subject to a relatively modest phase-out level, it will behoove taxpayers to actively work to keep their MAGI to a minimum where it reasonably makes sense to do so. One way to do this is to utilize Roth and HSA distributions rather than Traditional (pre-tax) account distributions if you find yourself bumping up against the phase-out threshold. Drawing on non-retirement accounts and cash assets also helps, as will keeping capital gains income to a minimum. Note that municipal bond income, which is generally tax-free, does not help – as this income is added back to your AGI to calculate your MAGI, and the latter is the number that matters here.

Those are the two main changes we want to highlight here today, as they are the most broadly impactful changes stemming from this new bill. However, parents, students, small business owners, Medicaid recipients, tipped workers, and those that earn overtime (amongst others) are also going to see some meaningful changes. If you are in those categories, we’re happy to explore the changes that are specific to you.

As with everything, the exact impact of all of this is highly personalized – and we stand ready to explore the numbers and planning opportunities as they specifically apply to you. Please reach out at any time to have these conversations. In the meantime, we’ll be fine tuning our well-honed tax planning spreadsheets to factor in these new layers of complication. Does the tax code ever get simpler? (and yes, that’s a rhetorical question).