Happy New(ish) Year. We’re now half way through January. No shortage of world events has already transpired, and next week ushers in a new administration. It’s never boring, and we’re grateful for the privilege of being on this journey with you. With the New Year also comes a bevy of new numbers (and policies) – for retirement accounts, gifting, taxes, and more. We wanted to highlight the ones most relevant to the majority of you. Here we go!

RETIREMENT CONTRIBUTIONS

401(k) and 403(b) contributions

Employee max = $23,500 (from $23,000)

Catch-up contributions (ages 50+) = $7,500 (no change)

- But here’s the kicker! If you will be age 60-63 at year-end 2025, you can now take advantage of an “enhanced” catch-up amount of $11,250 ($3,750 more than normal). This is new for 2025, and the legislative language is vague – but this is the best interpretation of the rules we have seen yet. Note that your company’s plan must be provisioned to allow for this extra amount, which it should be (but no guarantees).

Total employee + employer contributions to a 401(k) or 403(b) = $70,000 (plus any catch-up amount permitted).

- This is most applicable to those who use the “mega backdoor” methodology or who are self-employed and able to max out both sides of the equation.

Traditional and Roth IRA contributions

Max contribution = $7,000 (no change from 2024)

Catch-up contribution = $1,000 (no change from 2024)

- As before, your ability to contribute directly to a Roth is limited by your Modified AGI (MAGI) and your ability to make a deductible contribution to a Traditional IRA is limited by a combination of factors including participation in a workplace plan (by you and/or your spouse) and your MAGI. Contact us to learn more!

HEALTH SAVINGS ACCOUNTS

Individual max = $4,300 (from $4,150)

Family max = $8,550 (from $8,300)

Catch-up contribution (age 55+) = $1,000 (no change)

- Note that the catch-up contribution can only go into an account owned by the person age 55+. So, if you have a family account under one spouse’s name, you will have to open a second account for the other spouse when they reach age 55+.

- Remember that you can only contribute to an HSA if you have an HSA-eligible health plan, and you have not yet enrolled in Medicare Part A.

ANNUAL GIFT LIMIT

$19,000 (from $18,000)

We will soon publish a piece to help clarify some of the many common misunderstandings about this key planning tool.

ESTATE PLANNING

Federal unified gift/estate tax exclusion = $13,990,000 (from $13,610,000)

State of WA estate tax exclusion = $2,193,000 (no change since 2018!)

The federal limit, as shown here, is set to expire at the end of 2025, at which point it will revert back to “pre-Tax Cuts and Jobs Act” levels (indexed to inflation). Efforts are underway to extend this provision along with most or all other provisions of the so-called “Trump Tax Cuts.” More on this in the conclusion.

SOCIAL SECURITY

Wage limit = $176,100 (from $168,600)

This is the maximum compensation subject to Social Security taxes (6.2% for employees, 6.2% for employers). Note that Medicare taxes (1.45% each side) are applied to an unlimited amount of earned income.

For those of you currently receiving Social Security benefits, you received a 2.5% cost of living adjustment for 2025. However, the thresholds at which your SS benefits are taxed at different rates have not changed. If you are working and receiving SS benefits, your maximum earning before SS benefits are reduced has been increased modestly to $23,400 (applies until you reach your full retirement age (FRA)). Contact us for further guidance on this nuanced rule.

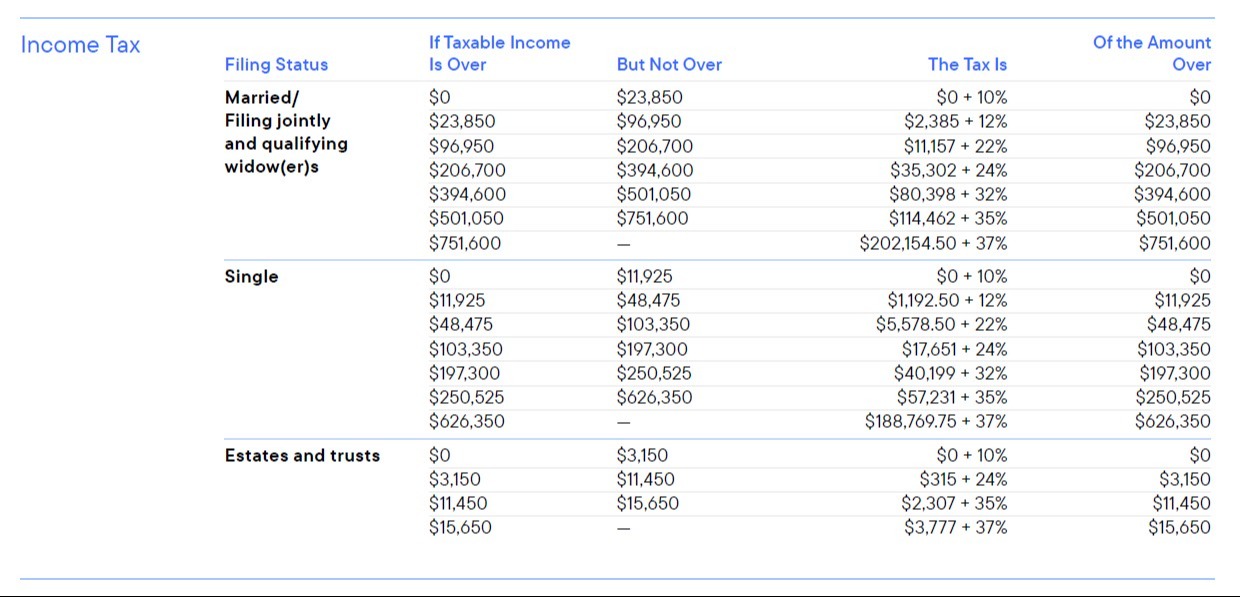

TAX BRACKETS

All tax brackets have been adjusted upwards to account for inflation, so you may see your paycheck grow slightly even if your wages haven’t changed. Here is a screenshot showing the most commonly used filing statuses. Consult with us or your tax advisor for further details.

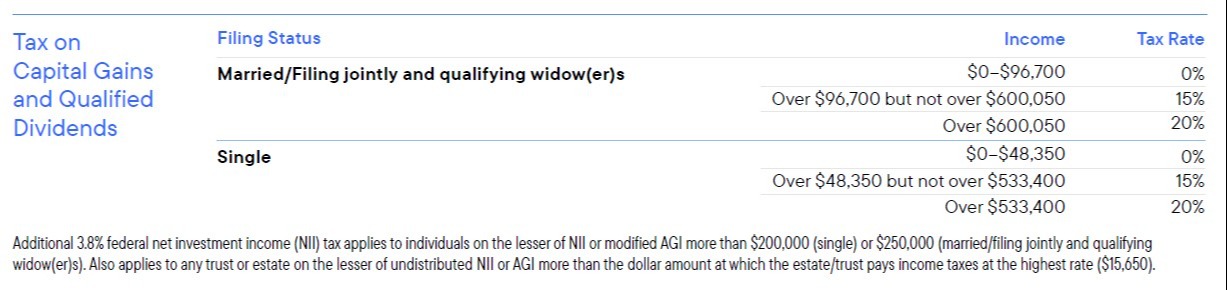

Note that the thresholds for differing long-term capital gains tax rates have also increased. Here are those numbers.

The standard deduction has also increased to $15,000 (single) / $30,000 (married, filing jointly), with additional amounts for those age 65+ or blind.

WRAPPING IT UP!

As you might imagine, there are way more numbers out there pertaining to any of the thousands of provisions in our wildly complex tax code. We’ve hit here on the ones we see most often for our clients, and we welcome your questions about anything that may not be seen here.

Lastly, we’ll be keeping a close eye on the potential expiration or extension of the so-called “Trump Tax Cuts,” most of which are currently set to lapse at the end of 2025. Such a lapse would have a material impact on the financial plans of many of you, and we have the tools to help illustrate this impact. Please reach out if you are concerned or simply have questions. We look forward to a great year ahead, and thank you again for the privilege of being able to help guide you through your financial decisions, both big and small.