Nothing in the global world of finance is easy. They are complex systems that are connected to each other through various means. So, although we mostly focus on US inflation and interest rates, it’s important to know that our interest rates are not in a vacuum.

Why is that? Because, if our interest rates are out of sync with the rest of the world, that will affect currency rates. Most of the world has been synced up both during COVID (cutting rates) and post-COVID (raising rates), except for Japan. Japan has been the lone country keeping central bank rates at close to zero. That’s even in the face of rising inflation there.

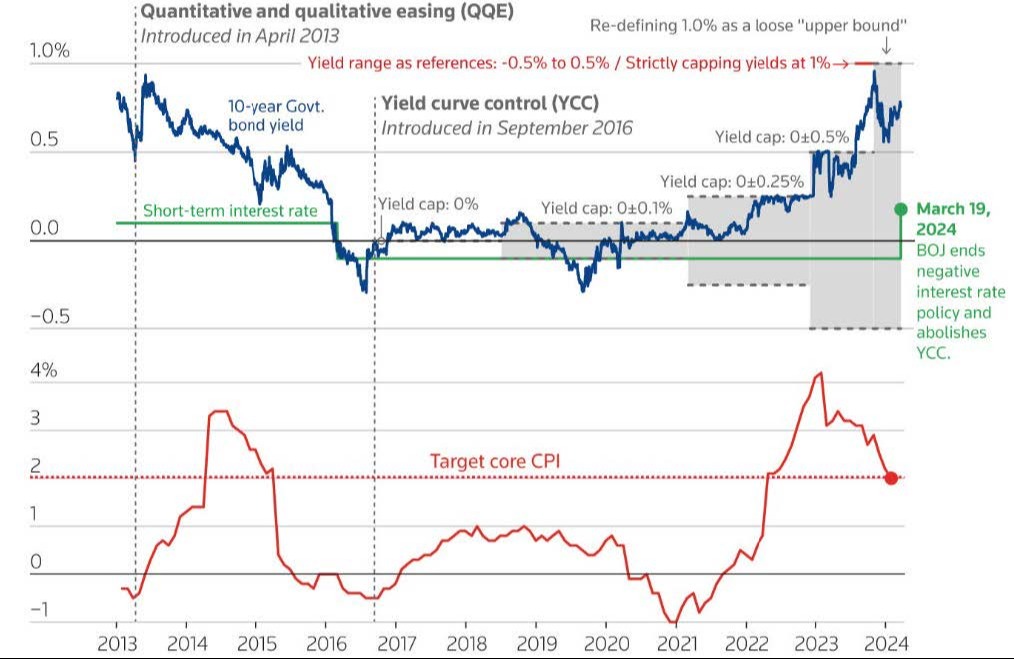

If you remember many months ago, I talked about global central banks talking from the same script, but specifically mentioned Japan as that lone central bank going their own direction. That was back in July of last year and the Bank of Japan has slowly moved off the nearly zero bound to a whopping 0.1% (but that isn’t the real rate, as the central bank will let rates go to 1% before intervening).

That’s a busy chart, but basically it is saying that Japan will let its interest rates float in a wider band than it has previously.

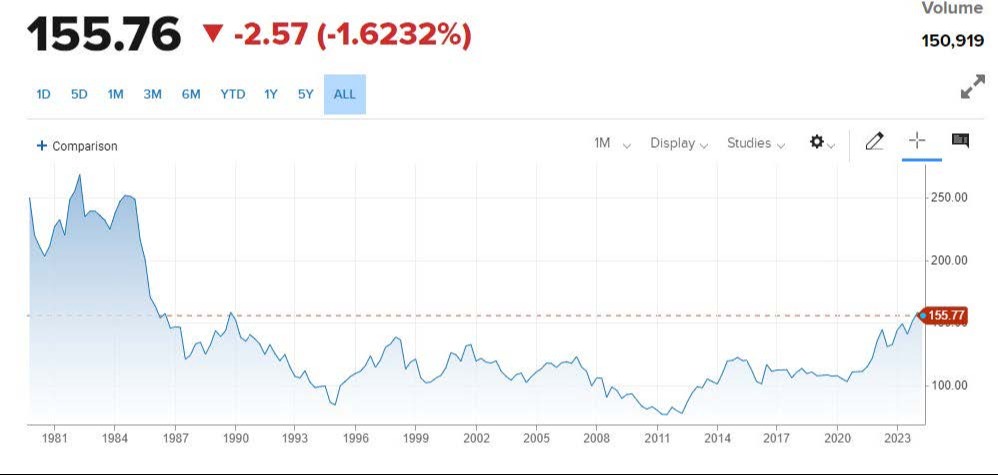

But remember I said that the global financial markets are interconnected and very complex. While the Japan Central Bank can continue to hold their interest rates down, there is a price to pay for that. That comes in the form of lower exchange rates. The Yen/Dollar exchange rate is the highest it’s been since the late 1980s.

Since that is an exchange rate, $1 buys 155 Yen. That of course could be a good thing or a bad thing, depending on what side of the trade you’re on.

If you are buying Japanese goods, they have become cheaper, but if you live in Japan (or using Yen) imports have become more expensive. That of course complicates the Central Bank’s problem. While trying to keep inflation down, they have now made all imports more expensive, thus pushing a portion of inflation higher.

On the flip side, all Japanese imports to the United States (and there are many) will become less expensive and will actually help our inflation rate. Now we know that services have been the sticking point for inflation, but a higher exchange rate will help on the margin. But what about the rest of the world?

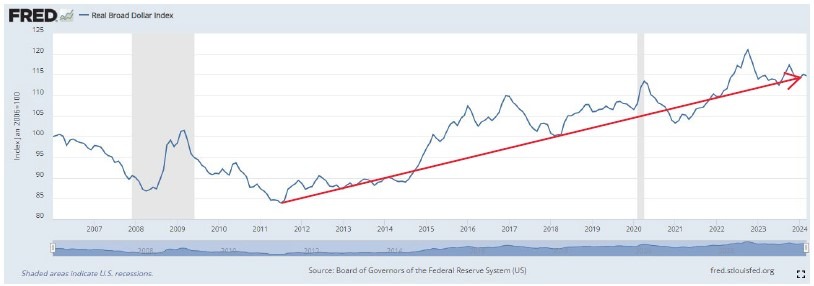

You can see from the chart below that the US trade weighted index has generally been going up since the Great Financial Crisis (2008-09).

A higher dollar will “import” deflation and “export” inflation. So, it’s a dance that all the central banks must participate in. As we are starting to hear that many central banks are considering cutting interest rates, it will be hard for the FED to be on the “higher for longer” island by itself. Because as we just noted, the higher US interest rates stay relative to other international rates, the higher the dollar will appreciate relative to those other currencies. While it’s good for the US to import all that deflation from other countries, those other countries are then importing inflation, which is contrary to the reason they are cutting interest rates in the first place.

If your head is spinning, you’re not alone. This stuff gets really complicated.

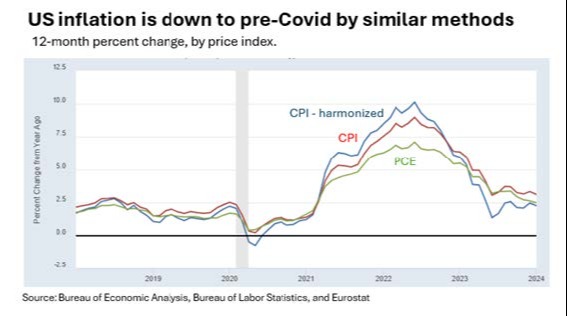

If you thought that Europe was doing a better job dealing with their inflation, you might stand to be surprised (as I was). Much of their inflation was related to energy costs and, come to find out, they don’t measure inflation the same way we do. Go figure!

If we measured US inflation the same as Europe, here’s what our inflation rate would look like now.

Inflation appears to be down to pre-COVID levels (blue line).

The FED is set to meet May 1st and we should see no change in their policy. We may however get a change in tone regarding “sticky” inflation, perhaps not coming down as fast as they would like. That may cause them to push off rate cuts to later in the year (or perhaps even next year). Of course, the market has already priced much of that in.

Meanwhile, on the earnings front, Facebook (Meta), Google (Alphabet), Microsoft, and Tesla have reported earnings for Q1. Meta was the stinker of the bunch and paid the price for it. Meanwhile, the rest have been better than expected.

As I mentioned last week, Apple and Amazon report this week, so we will see how those earnings reports look. Expectations are not very high for Apple, while the jury is out on Amazon.

That’s it for this week, I hope you have a good week. Reach out with questions or comments.