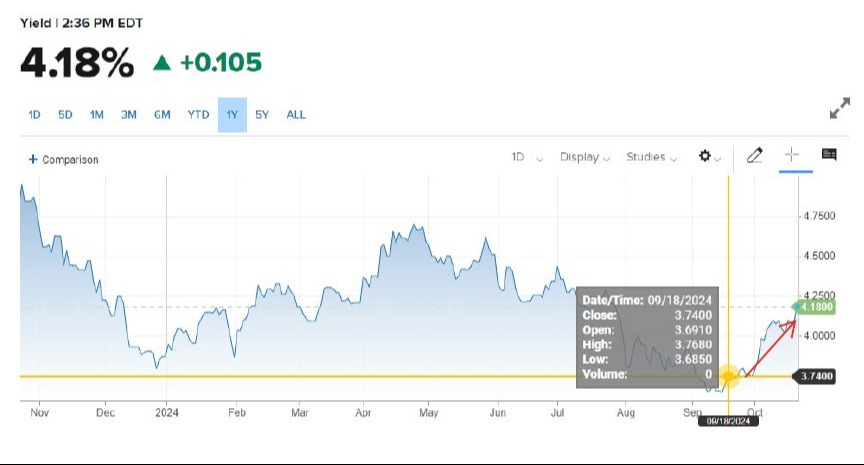

Interest rates matter, and they matter a lot when it comes to the market. So, to start today’s blog, let’s look at something interesting with regard to rates, and that’s how long-term rates have gone up since the FED cut rates on September 18th.

Today rates are at 4.18%, up from 3.74% at the close of business on September 18th (the day the FED raised rates). 0.44% doesn’t seem like much, but that’s increase of nearly 12%.

That is a reflection of some better numbers coming out of the economy of late. Is there more to come in regard to rate increases? Don’t know at this point, but let’s see some data that might provide some clues.

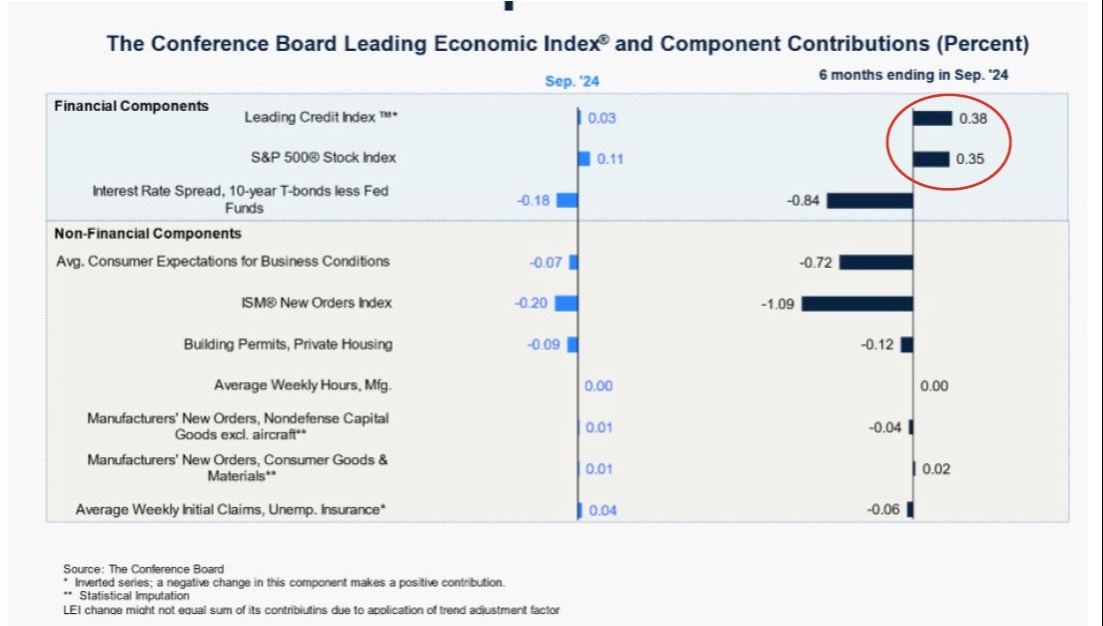

Here’s the Leading Economic Indicators (LEI) for the month of September.

Almost everything was either flat or negative for the month. And for the six month timeframe, the only things positive are the stock market and the Leading Credit Index, which looks at interest rates and spreads.

Let’s transition now to what the data and market pundits are telling us about what we can expect from “the market” in the coming years. We’ve looked at this at various points in the past, and it’s helpful to revisit it from time to time.

Goldman Sachs has come out with a new 10-year forecast for the S&P 500 and it’s pretty bleak. They think that the market-cap weighted S&P will average 3% per year, meanwhile the equal-weight is expected to outperform by 8% over that same period. You all know my opinion of Goldman Sachs, but let’s assume that they are right on this. I happen to think they will be right. Click here if you want to read the entire story.

Let’s take a look at the equal-weight versus the market-cap weight.

You can see that the outperformance from July has pretty much gone sideways since then and we are looking at a nice wedge pattern. Expecting it to either break down or break out. At this point we don’t know, but it is likely that the equal-weight outperforms in either scenario.

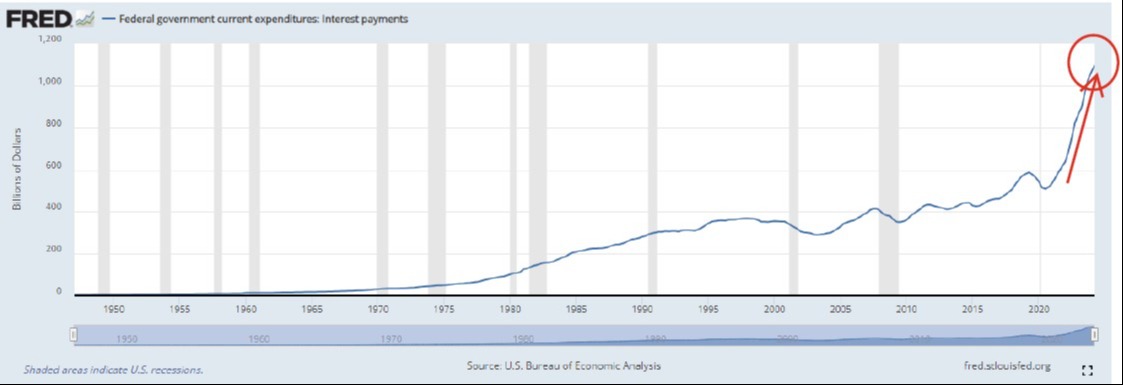

Looking at interest payments on government debt, you can see the big increase from both interest rates and the overall level of debt.

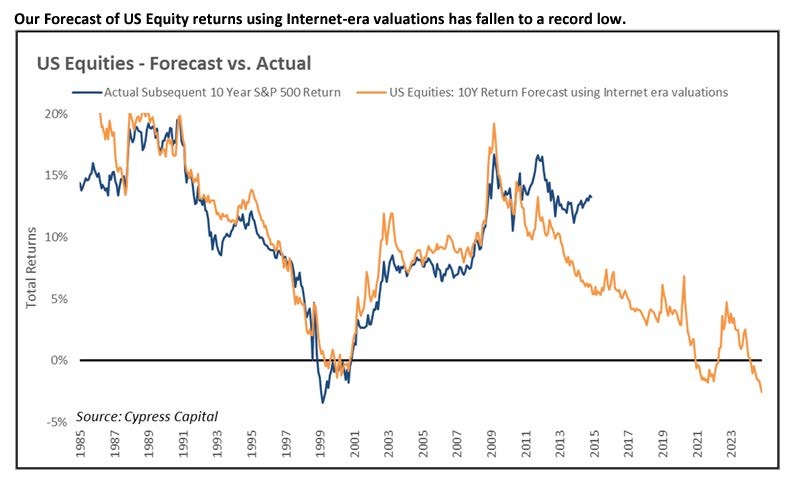

And finally, from our friends at Cypress Capital, a look at their 10-year forecast of returns from equities. In this, they look at current valuations as a means of predicting returns over the coming 10-yr period, as it is generally agreed upon that valuations are a terrible short-term trading signal but can provide a very useful long-term forecast of what to expect. You can see that their track record has been pretty good, although they seem to be a bit off over the last few years as valuations have stayed stubbornly high relative to historical norms.

Again, this would be for the S&P 500 market cap weighted, rather than the equal weighted. We would argue that there would be a difference between those two indices.

As we finish up this week, the teams are set. The last time we saw this match up was 1981. The New York Yankees and the Los Angeles Dodgers. Aaron Judge versus Shohei Ohtani. The two probable MVPs for their respective leagues. Shohei probably won’t pitch in this series, and Judge certainly won’t. It’s going to be fun. If you have any questions, please reach out and we will be happy to have a conversation.