It’s been a couple weeks since my last blog. Andrew took a week with a planning blog and last Monday was Memorial Day. I hope you were able to give thanks and remember those that have paid the ultimate price to keep our nation free.

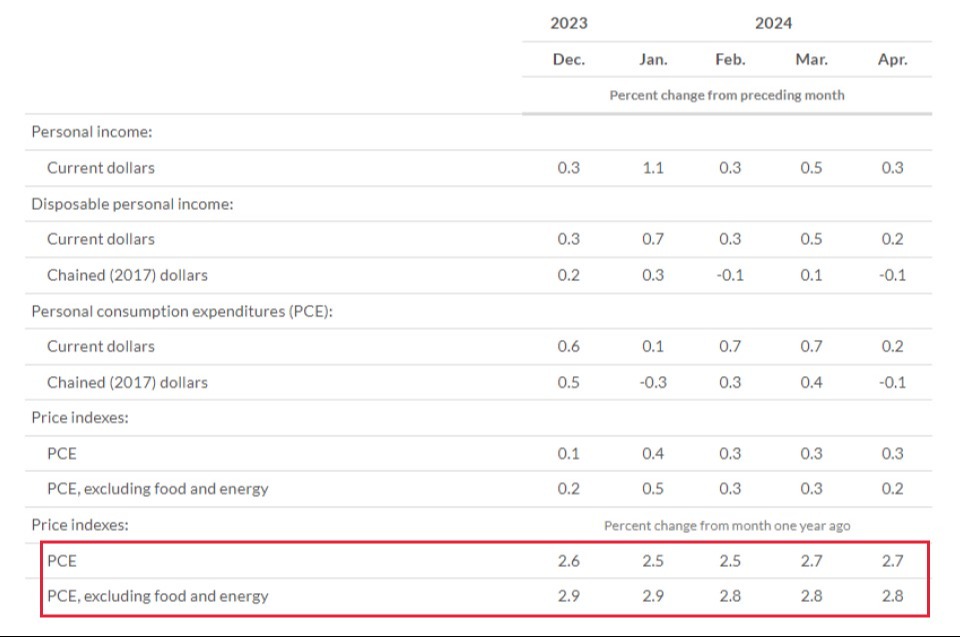

Last week, the Bureau of Economic Analysis (BEA) came out and said that the Personal Consumption Expenditures (PCE), which is the FED’s preferred measurement of inflation, measured in at 0.2% month-over-month for Core, and 0.3% when you factor in food and energy. Here’s how the numbers look on a year over year basis.

You can see at the bottom of the chart that we are hanging in the mid-2% range, just below 3%. You also know that we have been advocating for an inflation target that reflects the past 100 years, rather than an arbitrary 2% target. That would be more along the lines of 3%-3.25%. So long as the “fear” of inflation doesn’t cause people to either hoard or prematurely purchase things because of inflation being significantly higher in the future, that seems like a reasonable target.

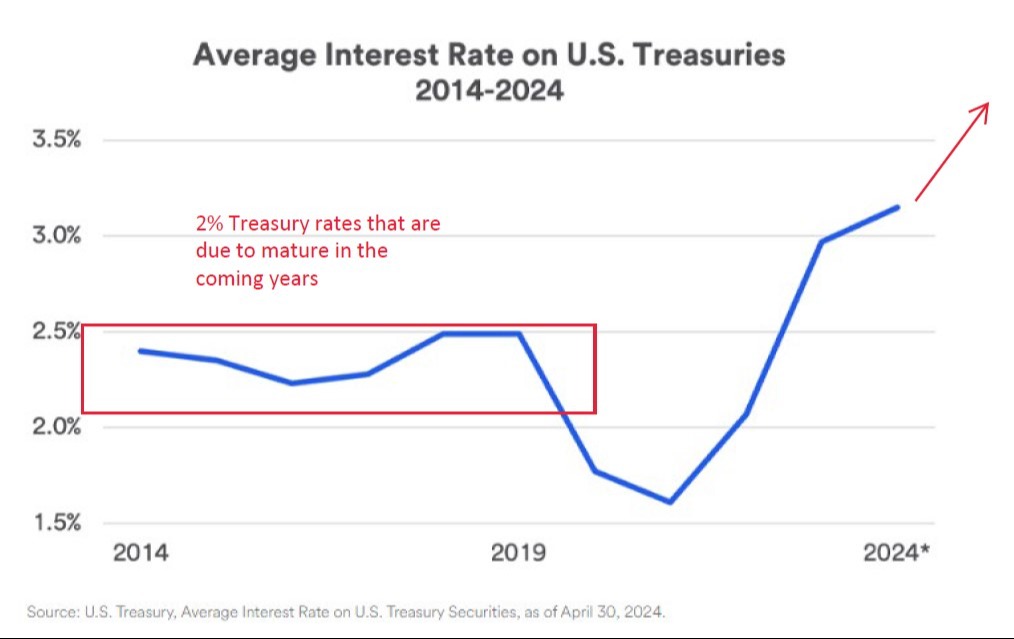

Of course, once you add a spread on top of inflation, so that investors of US Treasuries can get a “real” return above inflation, your expected rates should be somewhere in the 3.5% to 5% range, depending on maturity. In a normal world, that would seem very reasonable. The problem comes when you factor in the size of debt the US (and other countries) has accumulated over the last 20 years.

Some simple math would look like this: $34 trillion x 4% (average interest rate) = $1.36 trillion in interest that is due each year. That assumes we don’t continue to add to that debt (which we know the GAO is expecting $2 trillion more debt per year, through 2030). Here is a chart of the weighted average interest rate the US government is paying. Keep in mind that the longer rates stay high, the more of the old “cheap” debt rolls off.

So, if we add another $12 trillion to the debt over the next 6 years ($46 trillion in debt), the budget will require $1.8 trillion in debt service on a yearly basis, and counting…

Without spending cuts or more revenue (I mean taxes) we will keep adding to that total. We’ve gone through the numbers before, but something’s got to give.

According to the chart above, we are not at 4% yet, but 5-year T-Notes issued in 2019 will be coming due this year, as will 10-year Notes issued in 2014 and will have to be refinanced at a higher rate, so you can expect this average rate to continue to climb over the next several years (depending on economic health).

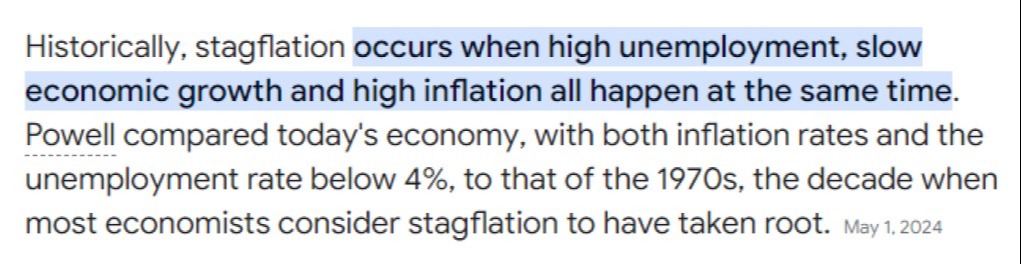

We also know that the more money that comes out of peoples’ pockets for taxes, the less they will have to spend in other places. That’s not political, that’s just a fact. Which would get us closer to the possibility of stagflation.

I think we are a long way from being in stagflation, but we have “higher” inflation and growth is slowing back to trend (likely sub 3%). The only thing not on that list is high unemployment. When speaking about growth, the government just came out with their second revision of GDP from the first quarter, and it was quite a downgrade.

1.3% is not exactly a hot economy.

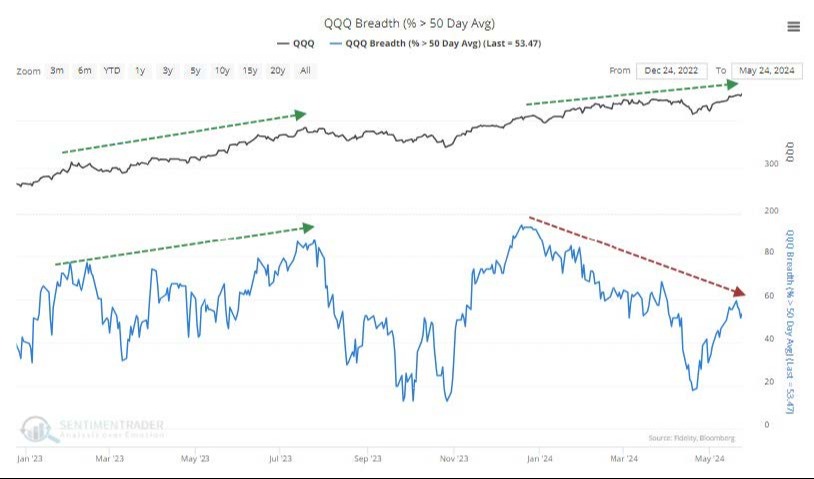

Finally, we have been noticing that the market is getting narrower lately. What does that mean? It means less stocks are participating in market appreciation. Check out this chart.

The pullback in the markets in April pushed the number of stocks above their 50-day moving average to less than 20%. In May, many have rebounded above that level, but it looks like it may stall here below 60%. You can see how the chart looks above. A downward sloping line as compared to an upward sloping line in 2023. That’s called a divergence and typically not a good thing. Does that mean the markets are going to fall apart? Not necessarily.

It does probably argue that the market will have to work extra hard to make new highs. Here’s the chart of past times this has happened.

It shows that over the next couple months things are mostly mixed but look out 6-12 months and things look better.

We can also look at the Nasdaq 100’s 200-day moving average (the longer-term perspective).

It too shows a divergence similar to 2021, which preceded a decent pullback in the markets. In fact, it’s only the 3rd time in the last 30 years that both the 50-day and 200-day showed divergences. Here’s what that looked like.

Granted, that’s a small sample size, so take that with a small grain of salt.

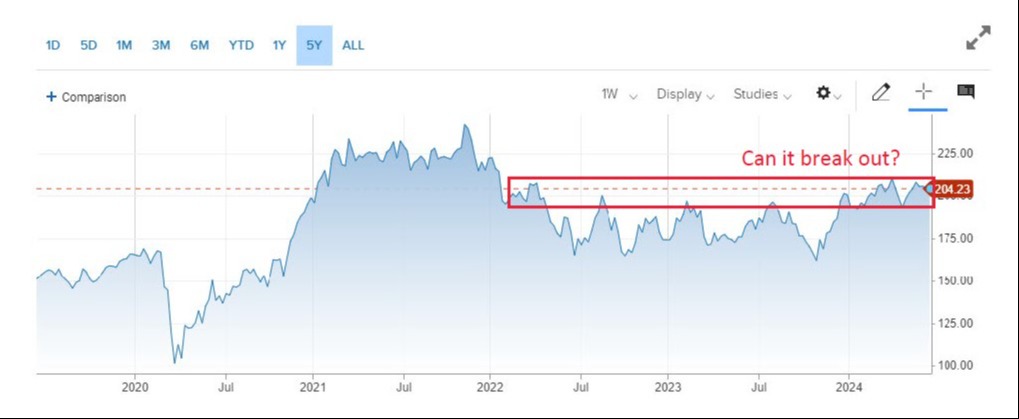

As you know, we have been hoping that the markets would broaden out and that would be a sign of a healthier economy. We have had fits and starts, but it has not gained steam quite yet. Here’s a perfect example, the Russell 2000 (small cap stocks).

They are trying to get off the mat, but so far have not achieved escape velocity. And we are at historical valuation spreads between large and small companies. We will have to see how that plays out.

That’s it for this week. The west coast is supposed to have a massive heat wave, hard as that may be to believe as you look outside right now. 110 in Vegas, 100+ in Sacramento. I hope you have a good week stay cool if you can. Reach out with questions or comments.