Big news over the weekend that President Trump said he would nominate Kevin Warsh as new FED chairman to replace current chair Jerome Powell. It’s not news that Trump has had his issues with Mr. Powell, primarily because he has not acquiesced to the President’s demands to more rapidly lower rates.

Keep in mind that President Trump nominated Powell for that position back in 2018 to replace then chair Janet Yellen, with Warsh being set aside at that time. Now Powell is on the outs and Kevin Warsh is the new guy.

It’s no question that I’m not a fan of the Federal Reserve. For lots of reasons, but mostly because they seem to try and micromanage the economy with their use of interest rates, instead of using the other tools they have.

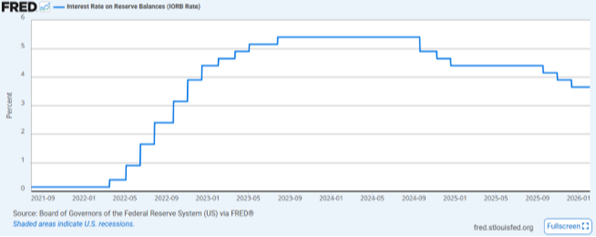

A couple of their big tools are the ‘reserve requirement’ and ‘interest on reserve balances’ (IORB). The former causes banks to hold more securities on their balance sheet and therefore not lend out as much, which in theory slows down the economy (and vice versa if they lower the reserve requirement). Today the reserve requirement is ZERO (has been since March 2020), meaning banks don’t need to hold a percentage of their deposits as reserve (talk about fractional reserve). The latter refers to the amount that the FED pays to member banks for their reserves held at the FED. This tool has become especially important since the reserve requirement was eliminated, as it now serves as one of the primary ways the Fed influences bank behavior and overall money market rates. Controversially, this currently has the FED running a massive deficit by way of paying billions to banks (makes you wonder who they are really serving, the people or the banks).

Today, the Federal Reserve is paying banks 3.65% to “park” money with the FED (via the IORB). Here is a chart showing the last five years.

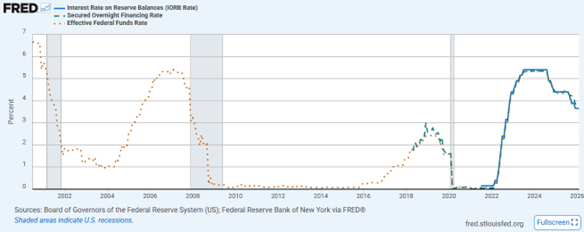

You can see that the FED was paying over 5% for money. Here’s a longer look at this rate.

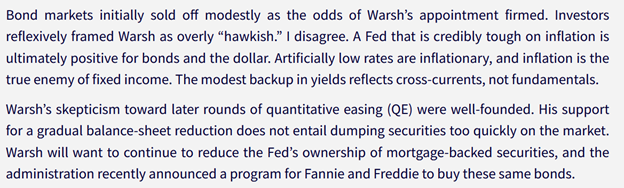

Getting back to Kevin Warsh, he could possibly be a reason for me to believe in the FED again. Why is that? Let’s take a few bits from Professor Jeremy Siegel (read in full here). Markets immediately sold off thinking Warsh might be too “hawkish”.

I agree, the FED should be the “lender of last resort”, but too often has been the first one to the table. It’s ok to allow the markets and economies to ebb and flow and to occasionally have a reset. Better to have small resets than one BIG one. Coming out of the 2000-2002 bear market and 9-11 – those are decent places for the FED to intervene. Even stopping 2009 from getting worse is reasonable. But having that linger for years, and now mostly for decades, doesn’t seem reasonable to me.

Finally, Professor Siegel ends with this.

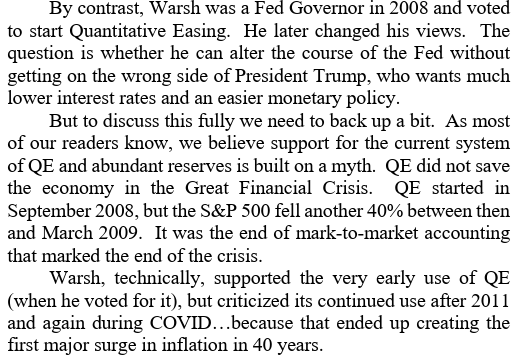

And finally, from our good friend Brian Wesbury from First Trust. A bit of history when Kevin Warsh was a FED governor (not the Chair).

This I agree with 100%!

Here’s a quote from Warsh back in 2011.

And one final thought from Brian.

Brian Wesbury was a big proponent in 2008 of the need to stop “mark to market” accounting. In his eyes that was the turning point in the markets. It’s hard to argue with that, take a look at the following chart. The green “M2M” dot marks where “mark to market” accounting requirements were lifted. The FED should have let the “patient”, the economy, survive on it’s own once the immediate crisis was over.

Doing less is sometimes doing more. In the case of the FED, I think that is definitely the case. No need to continue to run the car from one ditch to the other. In the words of Wayne Gretzky, skate to where the puck is going, not where it has been. With any luck, Kevin Warsh will be that kind of FED Chair.

That’s it for this week. If you have any questions or comments about this or any other topic. We will certainly be happy to have a conversation. Oh, and Go Seahawks!!!