With a stroke of a pen on May 20, 2025, Gov. Ferguson signed into law a set of substantial changes to the estate tax rates and exemptions here in Washington. This was part of a broader set of tax increases, including changes to the capital gains tax that were in the same bill as these estate tax modifications (more on this change at the end).

We spend considerable time here at MPCA educating clients on the Washington State estate tax – as it hits an increasing number of people and is also nearly completely avoidable with good planning. These new changes are meaningful, and they further emphasize the need for and value of this good planning.

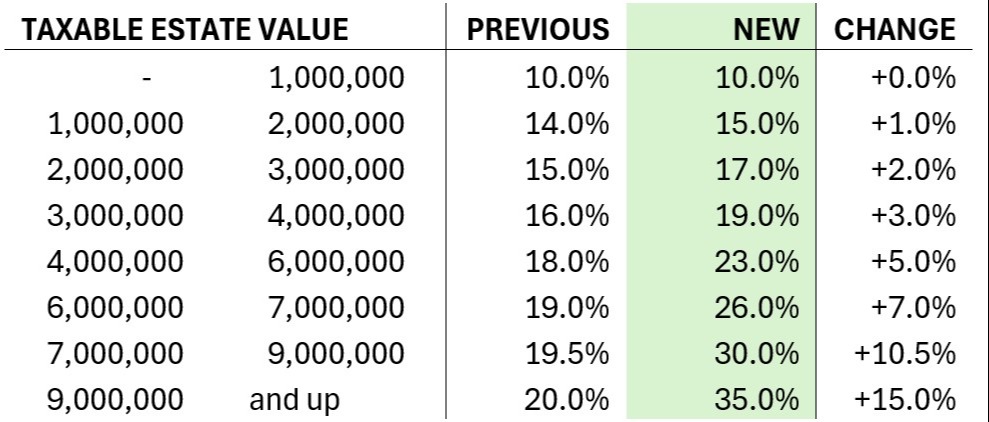

To understand what’s new, it’s helpful to understand what has been. Washington is one of handful of states that taxes estates. Every individual receives an exemption, previously equal to $2,193,000. Any estate value above this exemption threshold is taxed based on a progressive rate schedule (10-19% previously). So as to not “bury the lead,” here’s a peek into the new changes. We’ll follow this with a discussion of how this might impact you, and how this further emphasizes the value of good planning.

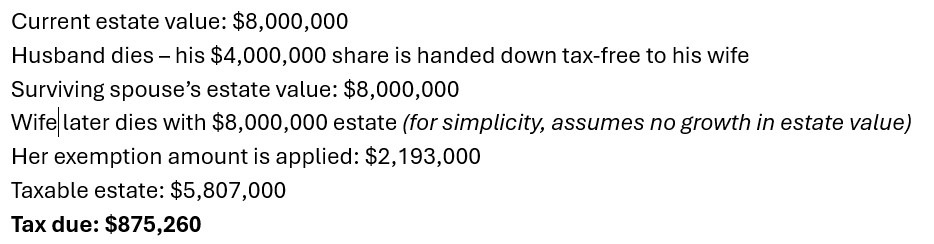

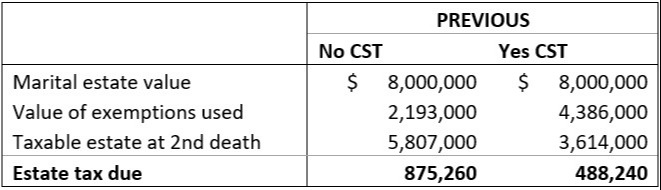

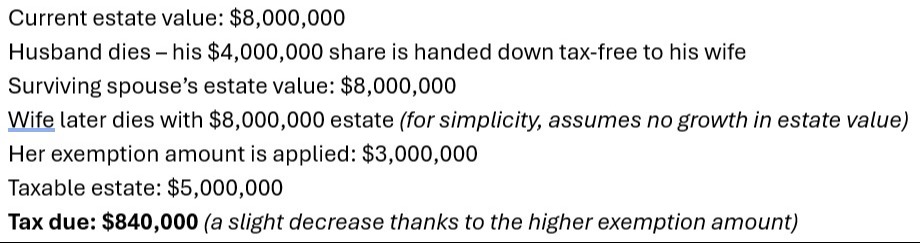

So, how does this all work and why does it matter? Let’s set the table with a basic understanding of how the tax structure works here in Washington. Admittedly, this is a simplified version for the sake of illustration, and we invite you to reach out for a more nuanced discussion specific to your circumstances. We’ll start with an example of a married couple with a total estate value of $8,000,000 prior to the death of the first spouse.

Here in Washington, a spouse can pass the entirety of their estate to their surviving spouse tax free, but they cannot directly pass down their exemption amount (unlike at the Federal level, where the exemption is “portable”). With no advanced planning for estate tax considerations, here is how things would shake out for the couple in our example:

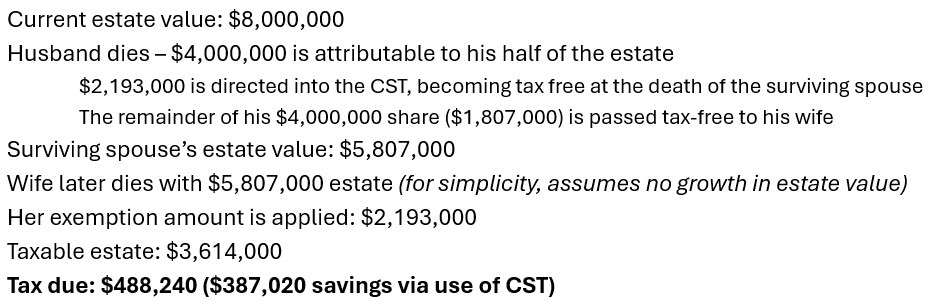

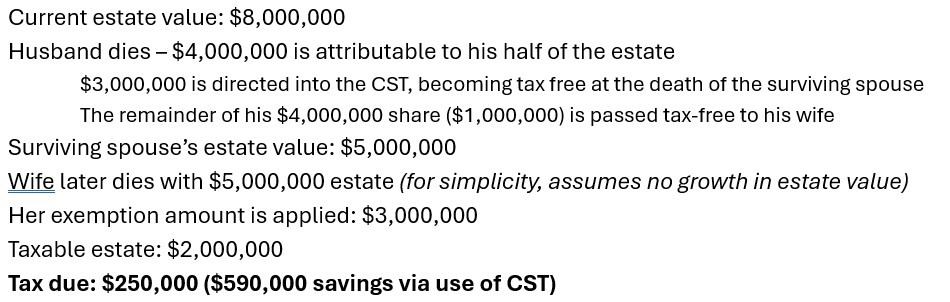

Now, if that same couple had engaged in advanced estate tax planning prior to the husband’s death, they almost certainly would have utilized what is called a “Credit Shelter Trust” (CST) (aka, “Disclaimer Trust” or “Bypass Trust”). This technique enables the first spouse to effectively transfer their exemption amount to the surviving spouse. We’ll spare you the details of the mechanics of these Trusts for now and instead focus on the tax impact. Here’s how that same situation would look if the CST was used:

Now, let’s see both of these scenarios with the new (higher) exemption amount and the new (higher) rates applied. As before, we’ll start with no use of a CST:

Now, let’s assume that the couple spent some time with their estate attorney and utilized a CST to help mitigate this tax:

In this example, we can clearly see a few things:

- The increased exemption amount will help reduce the estate tax burden here in Washington. In fact, in this example, the estate tax due was decreased in both scenarios. In fact, the increased exemption amount (now indexed for inflation) may negate the need for advanced planning for many, while significantly increasing the need for others.

- The value of a Credit Shelter Trust has increased meaningfully, as you are now looking at being able to exempt at least $6,000,000 from estate taxes, rather than $4,386,000. Not only is this a larger number in absolute terms, but it becomes more meaningful when you realize that it is being applied against higher marginal tax rates (up to 35%, as seen above).

- The increased rates will meaningfully impact the tax bill on high value estates in a negative way. I’ve included a table below that shows the numbers for a $16,000,000 marital estate, double the value from the example shown above. You’ll see that the estate tax jumped 35% between the two “No CST” scenarios ($2.45MM to $3.33MM). It even increased in the “Yes CST” scenario, but by a much smaller percentage (further highlighting the importance of good planning).

There is so much more than can be written about all of this, including:

- What are some ways beyond the CST to help mitigate your estate tax exposure here in WA?

- How should you think about this if you are single or already widowed?

- If you already have a CST in place, do you still need it with the exemption amount being so much higher now? What options are available if you don’t?

- How does a CST really work anyway?

We certainly have our work cut out to update all of the previous materials we’ve published about estate tax planning here in Washington. We’ll be working on those and will make them available when they are ready, but wanted to get this introductory piece out to you now so that you can start thinking about this and asking questions of us and your tax and estate professionals.

HOW ABOUT THAT CAPITAL GAINS TAX INCREASE?

At the beginning of this piece, we noted that the estate tax changes were part of a bill (SB-5813) that also increased the capital gains tax here in Washington. Previously, long-term capital gains exceeding $270,000/yr (2024 threshold, is adjusted annually for inflation) were taxed at a rate of 7%. Under the new rules, gains exceeding $1,000,000/yr are now subject to a 9.9% rate. This is retroactive to January 1, 2025. It is unclear if this $1 million threshold will be indexed for inflation in the same way the lower threshold is, though it appears to me that it is not. We can hope this will be corrected in the next legislative session.