I’ve been instructed to keep this rather short. Andrew and Sara-Anne welcomed their new baby last Tuesday, so my publisher is on restricted work duty (if you know what I mean). Congrats to Brady Ellis Barfoot and his parents.

So, in order to live up to my obligations to keep this short, we all would welcome questions regarding any or all of these issues, rather than try to answer them all here.

One glance at the headlines this morning and the charts today and you’ll see the markets seem worried. Here are the things the market is concerned about:

- Possible recession and the FED being behind the curve

- Japan “carry trade” and rising Japanese interest rates

- The coming presidential election

- Potential broadening war in the Middle East

I’m going to take the easy ones first. Yes, there is the potential for a broader conflict in the Middle East and nobody, including me, can really predict how it unfolds. My guess is it will escalate, and that escalation will largely depend on how NATO and Russia/China keep things in check. But it has the potential to get out of control at any time. What’s even more unknown is how much it would impact markets over various timeframes.

The presidential election? I’m not going to comment too much on that, other than to say that policies will largely continue, and we will continue to head down the road towards the ‘Fourth Turning’ climax. For those who haven’t read Neil Howe’s book, I highly recommend it. His work suggests that the world continues on more or less the same path until something happens that causes an existential threat. At that time, the US population will come together to fight that threat (whatever it is). The last one was Pearl Harbor and WWII. Before that was the Civil War – so these things don’t happen often! It doesn’t have to be war. It could be a financial crisis or another pandemic, maybe aliens are real and they invade us! Too far?

Let me handle the recession and the FED. If you have read any of my weekly pieces over the last four years, you know that I don’t hold the policy makers at the FED in the highest regard. I frequently cite the analogy of running the economic “car” from one ditch to the next. If you read my piece on July 8th (click here), I sort of mocked Michelle Bowman for her June 21st comments on being open to raising interest rates! That was six weeks ago, and she was still in the camp of raising rates? Come on!

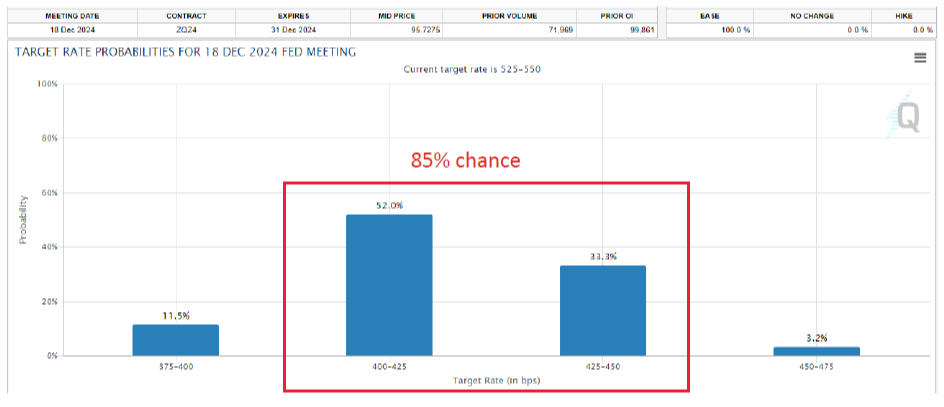

The following week I mentioned the odds of a FED rate cut through the end of the year. Three weeks ago, the odds were 90% that there would be between two and three cuts (0.50% - 0.75%). Let’s look at where they are now.

There is now an 85% chance of 1.25% - 1.5% cut in FED funds rate by year-end. That’s a huge move in just a few weeks. Oh, and by the way, we’re back to where we were at the beginning of the year (in terms of rate predictions). Go figure. In the meantime, the FED is going to bang up the fenders a little as they scrape along the ditch (no tow truck needed, this time). In the interim, the markets will try to sort out what they expect this all to mean for the economy and company profits. Such sorting normally equates to volatility, just as we’re seeing currently.

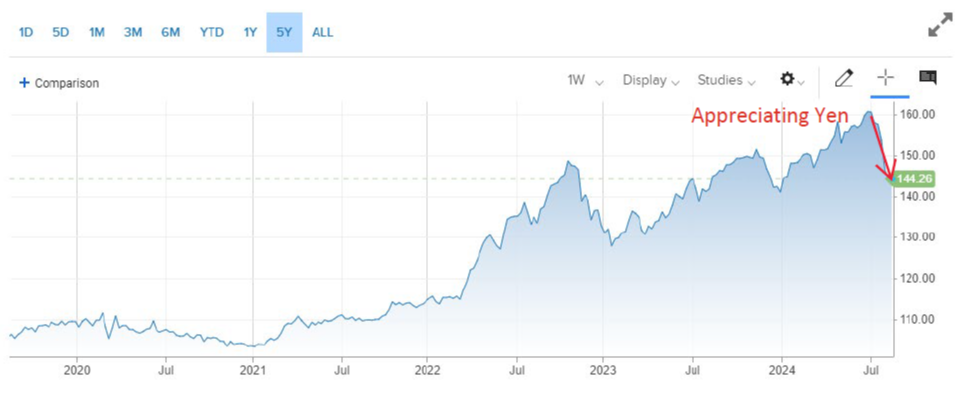

Finally, there is the Japan “carry trade.” If you’re unfamiliar with that, it is borrowing in Japanese Yen and investing somewhere else in the world (most times in the US). You would do that because interest rates were at zero and the currency was weak, so you could pay back those funds with cheaper Yen. Well…until it doesn’t work anymore.

Here’s the chart of the Japanese Yen over the past few years.

When the line goes up, the US Dollar is strong. When the line goes down, the Yen is stronger. In general you can see that the dollar has been getting stronger over the last couple of years. That appears to be changing with the US economy slowing down and on the verge of cutting interest rates, while the Japanese central bank is raising rates. They are out of sync the opposite way now.

So, I think a lot of this is an unwind of the carry trade, and that won’t go on forever. In the meantime, the Japanese stock market is down over 20% in the last week. Much like the Middle East, this has the ability to burn out of control and be a real problem (but in a very different way with significant differences in ramifications). If such disarray persists, the FED and other central banks will pull out that famous hammer from their tool bag (you know, the bag that only has one tool!). Then the FED will start banging away at the problem with lower interest rates and easier monetary policy, just like every other time in the past.

As I’ve said before, it will work until it doesn’t work and then we have a real problem. Just because we say the FED has beaten inflation doesn’t mean inflation can’t come back. As a matter of fact, I believe it will come back because of the rate cuts and easy money. My dad always said, don’t cause an accident to prevent an accident. That’s exactly what the FED will do. The inflation problem will come out again because they are using the only tool they have and that is to stimulate demand when it is low and pull back on demand when it is too high. That worked well for 40 years when productivity and natural disinflation was the norm. Now we can’t have disinflation without deflation. Disinflation is good, deflation (in the eyes of the FED) is bad. I would disagree with that, but what do I know!

Ok, about a thousand words and only two charts. Objective fulfilled. If you have questions or want more in-depth information about these issues, please reach out and we are all happy to have that conversation. I hope you have a good week.