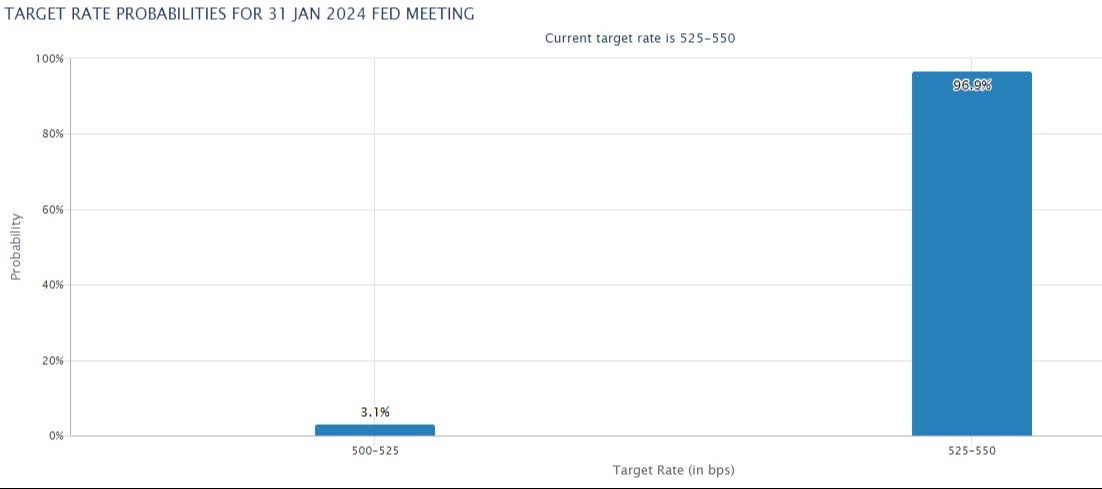

On Wednesday we have the first Federal Reserve meeting of the year. The market expects it to be a nothing burger (a very academic term, for sure). The FED is expected to keep short-term interest rates at 5.25% to 5.5% at this meeting, as illustrated in this chart.

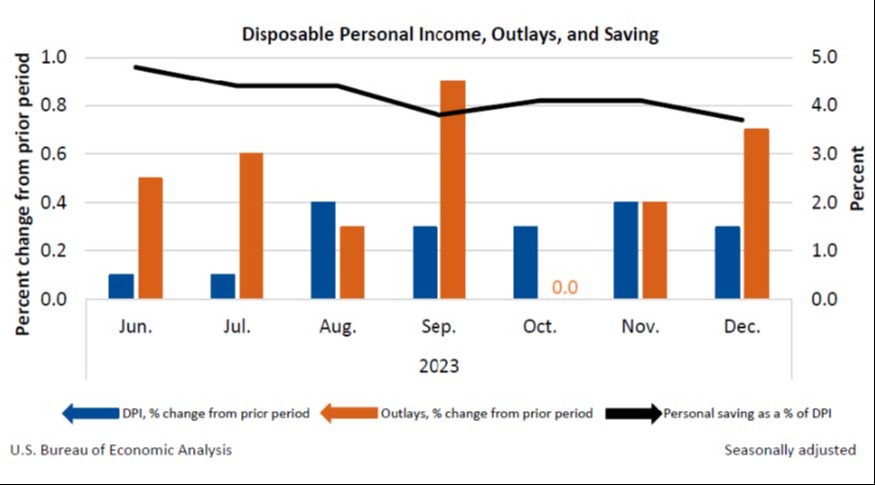

And that sort of makes sense. The economy seems to be doing ok, with spending continuing to outperform regardless of overall indebtedness. Of note, you can see from the chart below that the savings rate continues to decline.

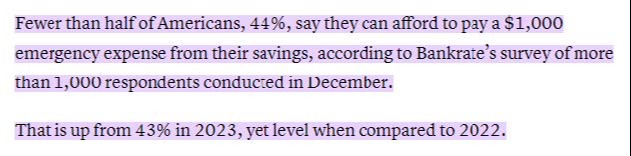

Meanwhile, an updated study from Bankrate shows that less than half of Americans can afford to pay for a $1,000 emergency.

So let me get this straight. Unemployment is close to all-time lows (we will look into that more in a second), spending is up, savings are down and 56% of people don’t have $1,000 to cover an emergency? It’s an odd mix, for sure. Despite this, add in the ‘wealth effect’ of a higher stock market and things appear robust enough to keep the FED on hold for the foreseeable future (at least in my eyes). Or am I missing something?

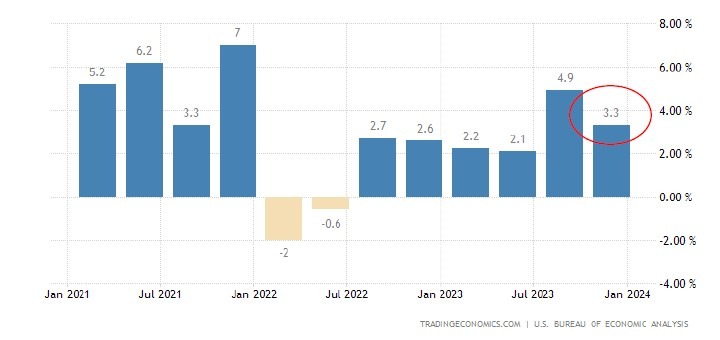

If you recall, the reason the FED had to raise interest rates was to slow down the economy in hopes of taming inflation. Remember, they can only affect the demand side. From where I sit, it doesn’t appear that the demand side has gone down much at all. GDP for the 4th quarter was reported last week and looked pretty good at 3.3%.

So, while the GDP is still robust, we have the FED’s preferred inflation index pretty close to that “magical” 2% level they’ve been targeting.

If you were to take a 6-month rolling number, we are already at 2%. So, what gives?

It’s this wonderful thing called productivity. Do you remember when you first started a job and you didn’t know anything? You had to be trained, learn your craft, and become proficient. That is the transition we are going through as an economy now. As the Boomers retire, they are replaced by Millennials (and younger), and they need to learn their craft and gain proficiency. Collective wisdom needs to be regathered. Think about it this way. You can hang drywall. It will just take you 15 views of the YouTube video, a few trips to Home Depot, a ton of wasted material, and more than a few pennies in the swear jar. Give it enough time and it will look good, especially if you strategically position the couch in front of your work! The professional can do the same in a fraction of the time, having shown up with exactly the tools, supplies, and expertise needed to get the job done (and done well) in short order. In many areas of the economy, we have the “YouTube learner” in jobs previously held by the entrenched expert. But eventually, with enough practice, that YouTube learner gets really good at the task. Productivity starts to increase. When this happens throughout the economy, investors can usually celebrate.

Seriously, it is possible to have robust GDP AND have low inflation. Let’s check out the productivity numbers.

Productivity growth was almost 5% in the 3rd quarter. No wonder corporate earnings continue to hang in there, even while inflation is coming down.

Let’s take a quick look at the employment numbers. It seems almost every month that jobs come in pretty good. See the chart below.

I’ll save you from doing the math, but without revised numbers for November and December, the economy added 2.7M jobs, compared to 4.8M in 2022 and 7.3M in 2021. Of course, many of those early jobs were the result of COVID layoffs and the economy reopening. It’s to be expected that job growth would slow as we get everyone back to work.

There are a couple of issues with the data. The first is headline jobs numbers are significantly overstated. We have mentioned this before, but for the 12 months ending March 2023, private sector jobs numbers were reduced by 358,000 while government payrolls increased by 52,000 for a net overstatement of 306,000 (25,500 per month). According to David Rosenberg, an economist, he estimates downward revisions for 2023 to come in around 443,000 (almost 37,000 per month).

The second issue is the continued low labor force participation rate. That measures the working age population from 15-64. We noted in the past that there is a historically large number of (mostly men) in that age group that are not counted as unemployed because they are not looking for work. Now, we can account for some that are close to that age 64 that are retired (that makes sense). There may also be some people that are disabled and can’t work, but there is still a large chunk where there is no explanation as to why they aren’t working. In case you were wondering how they pay their bills, that’s still somewhat of a mystery to me, although common sense would say family, inheritance, government assistance, and savings (or come combination thereof). By all accounts the savings part seems to have run its course.

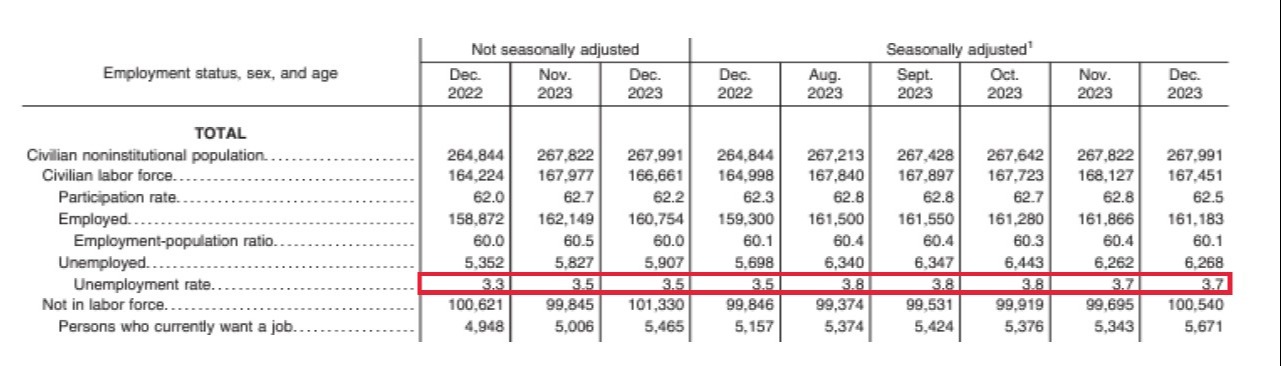

Here are some interesting stats when it comes to employment (apologies for the small print).

The civilian labor force is roughly 167.5M, of which 6.2M are unemployed as of December 2023. That gives us a 3.7% unemployment rate.

But check out the unemployment rate for those 16-19.

About 12% of that age group is unemployed.

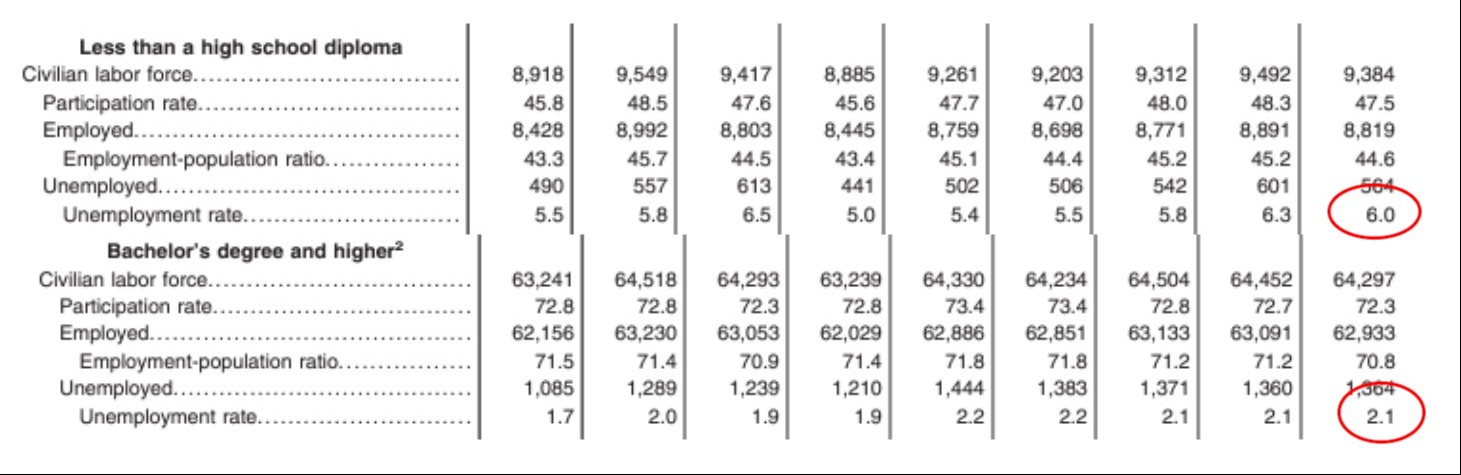

How about the difference between a college degree and less than a high school diploma.

The unemployment rate is almost 3x higher for those without a high school diploma versus a college degree. Almost twice as high for those with a high school diploma.

That might be a reason to go to college, but has anyone tried to hire a plumber, electrician, mechanic, or any number of jobs that don’t require a college degree? They are pretty tough to find, and if you do, they cost an arm and a leg. We can only hope that some of those in the 16-19 age group fill spots in some kind of trade. Good for them, good for the economy.

Keep an eye out for the next productivity number for the 4th quarter. My guess is that it will continue to be pretty good.

That’s it for today, I hope you have a great week. If you have any comments or questions, please feel free to reach out to us.