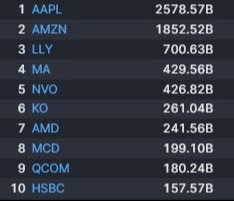

Let’s start with the big stuff. Big tech earnings are beginning to come out this week. Next week we should see the rest of the biggest tech names report. Here are this week’s biggest earnings reports (the numbers represent their market capitalization).

Next week we will see these companies reporting. A few more behemoths.

The only of the “Magnificent 7” not on the list is Nvidia. They won’t report until next month.

But this will give us a good idea of how earnings are holding up for the largest companies in the market.

Meanwhile, 78% of companies are beating earnings estimates so far this quarter.

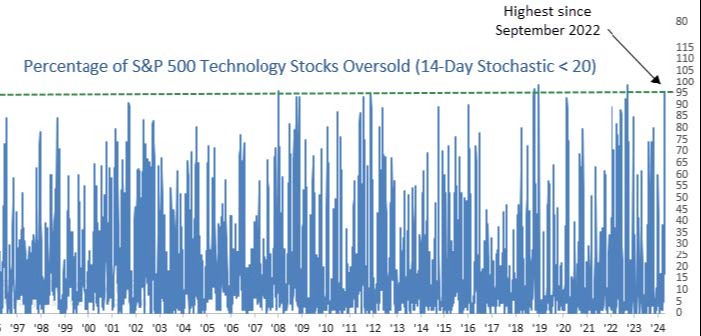

We have seen the market pull back over the last week or so and that is largely because of interest rates.

In fact, with this pullback in tech stocks, we are seeing a very oversold condition. According to SentimenTrader, this is the highest oversold condition for technology stocks since September of 2022.

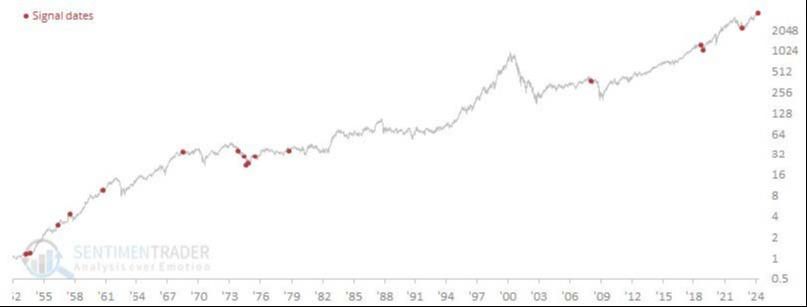

That’s a pretty chaotic chart above. Here’s the chart of just the times it exceeds that 95% level (red dot). It’s a rather infrequent occurrence, as you will see.

The biggest downsides were triggered during the ‘73/’74 bear market and the 2008 financial crisis. Only time will tell where this signal ranks.

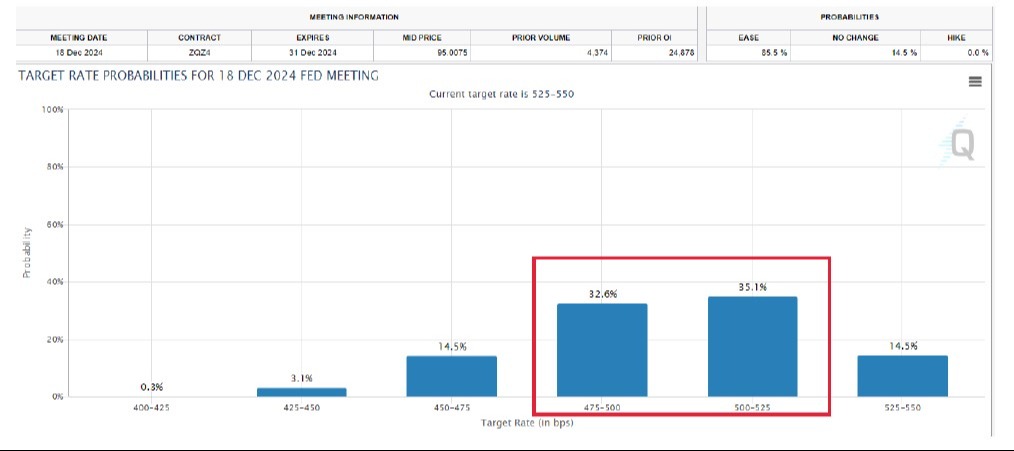

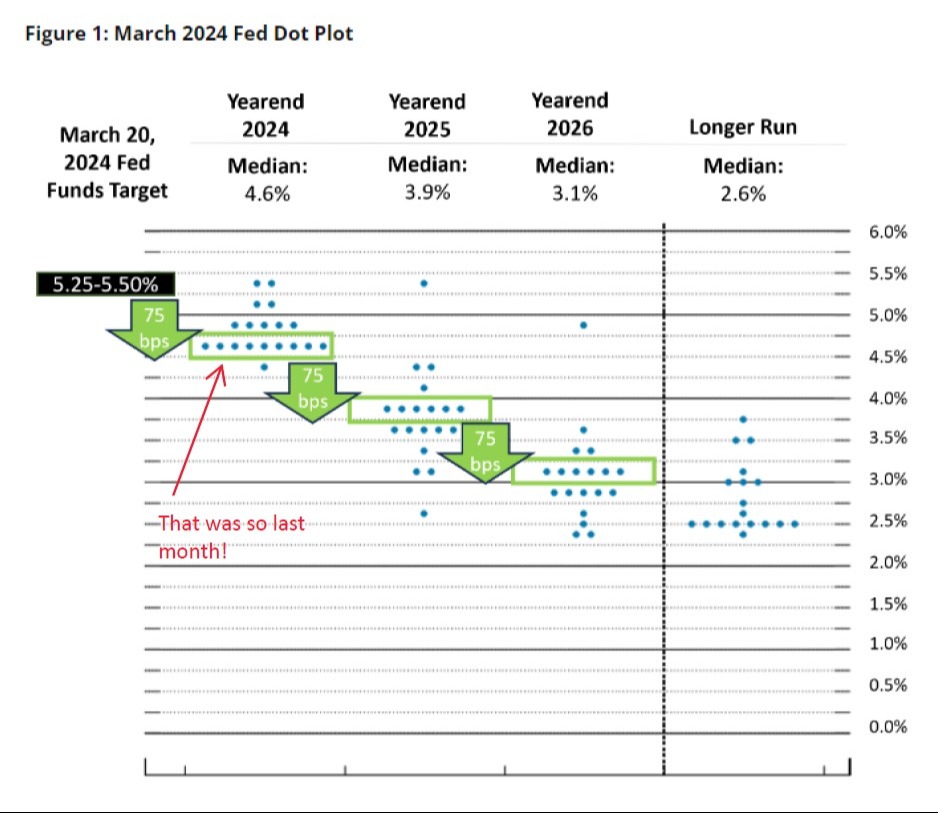

Like we’ve talked about before, higher inflation will cause rates to stay higher for longer. With the CPI that came out last week, the market has pulled another 1-2 rate cuts off the table for this calendar year. By year end, the market expects the FED to be between 4.75% and 5.25%, as you can see in the chart below.

That’s a far cry from the seven rate cuts the market priced in earlier in the year. It’s also a large reduction from the March FOMC “dot plot”.

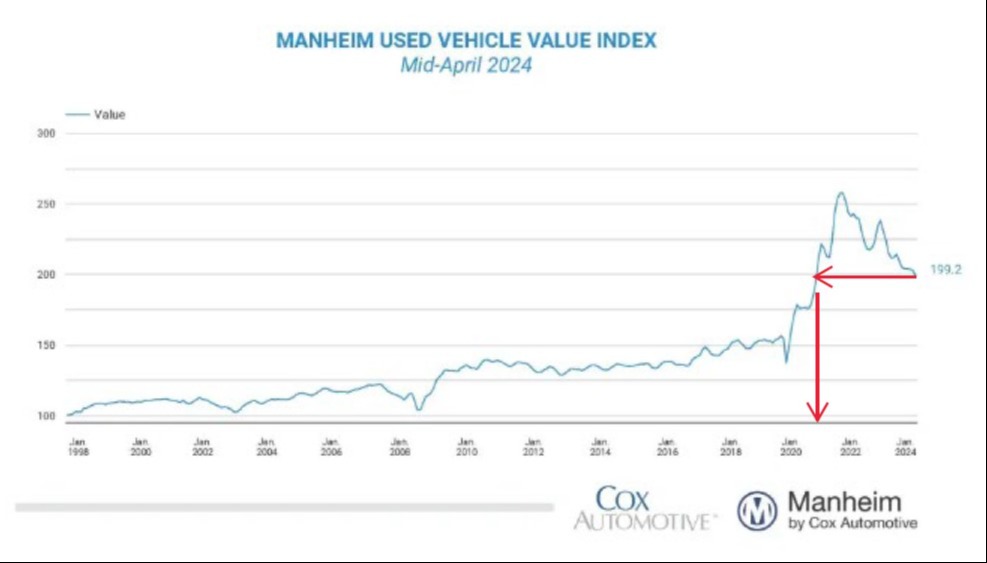

Now the question becomes, “Do we focus on the CPI or the PCE?” The FED has said their preferred measure of inflation is the PCE, while CPI is synonymous with inflation in the minds of the general public. Remember, the CPI reflects a larger component of shelter costs than does the PCE. We should get March PCE on Friday and we will see what that looks like compared to the “hotter” CPI. We know shelter is coming down, but last month’s CPI was plagued by shelter and car insurance. The latter seems to be, in part, a reflection of the cost of more expensive cars people bought during and after COVID, but the cost of cars and trucks are coming down fast! Seems like part of that problem will fix itself over the coming months, especially if the shortfall of mechanics can be alleviated, helping lower repair costs as well. That may take time! Here’s the latest Manheim used vehicle index.

We are now back to almost March 2021 prices for wholesale used cars. With a consumer that is extended, these numbers are likely to come down further over the next year. I would also expect that inflation would continue (at a much slower pace) to edge down towards 3% over the next year. The big wrinkle is government spending. If the U.S. continues to spend 5%-7% of GDP more than it has, that will by itself be inflationary. As I’ve mentioned before, that is an unsustainable path.

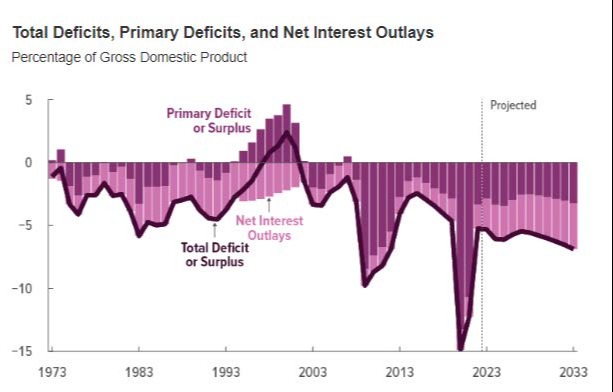

Here is a chart from the CBO (Congressional Budget Office), showing 60 years of deficits and surpluses. It doesn’t look good, and likely undershooting the target if we continue at this pace.

You can see the interest payments are more than the rest of the deficit. That’s scary to think about. If we had no interest payments, we would still have a 3%-4% deficit. We’ve really ramped that up since 2008, and even more after COVID.

That’s it for this week, I hope you have a good week. Let’s hope for a good PCE print this week. Please reach out with questions or comments.