We’ve discussed the tariffs many times in my weekly blog, but have we now finally solved the tariff issue? Does that solve some of the other issues, like $36 trillion in debt, a slowing economy, or higher inflation? Let’s explore. We’ll start with the second question before we turn our attention to the tariff news that has the market so excited today.

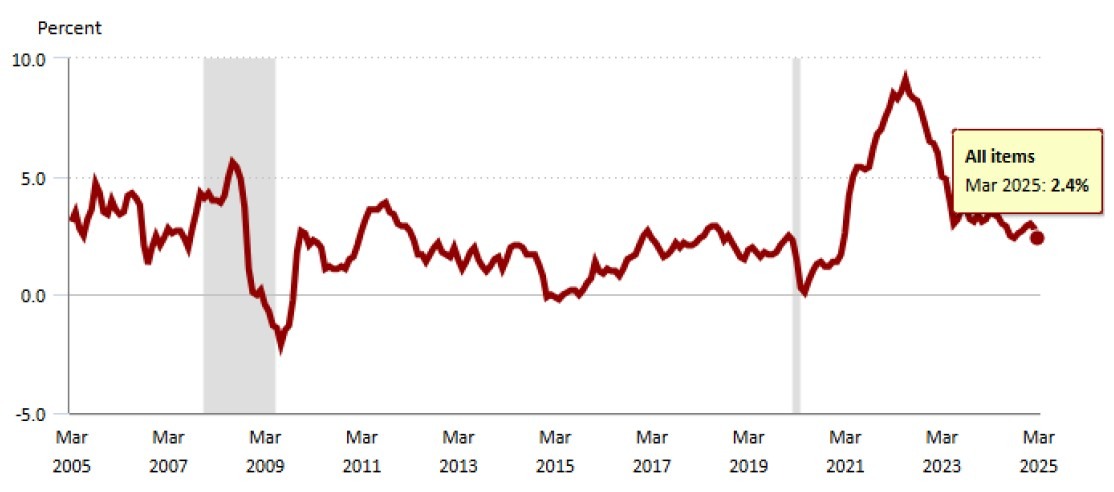

I spoke last time about tariffs being inflationary. I was also in the camp that tariffs will be ultimately reduced from the high levels that were introduced during “Liberation Day.” If we add all that together, I think tariffs will be marginally inflationary, but largely offset by a slowing economy. Let’s take a look at inflation.

It’s not as low as it was after 2008 and the financial crisis, but that was an abnormal time (in my opinion). We have also said that since the Great Depression, inflation has been around 3% to 3.25%. We are now below that level, and my guess would be we will remain somewhat below that level when taken over the next decade or two. That doesn’t mean that we won’t go above that from time to time over the next five plus years, but the trend should be our friend, generally speaking.

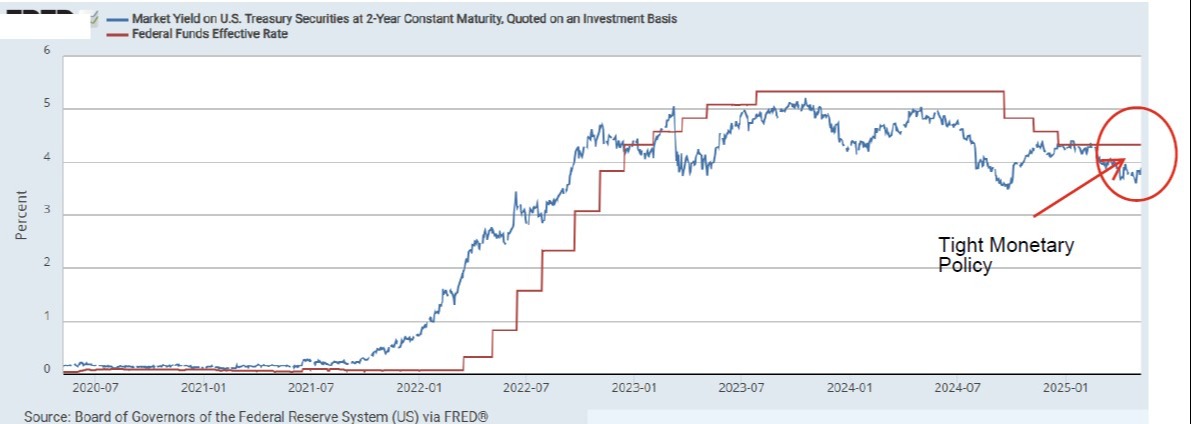

So right now the FED is ‘TIGHT’ on interest rates (red line is above blue line on the chart below), partially because they don’t want inflation to come back, but also because they have said (and I think they believe this), that tariffs are inflationary and are concerned about the level of tariffs moving forward. That typically points to a slowing economy.

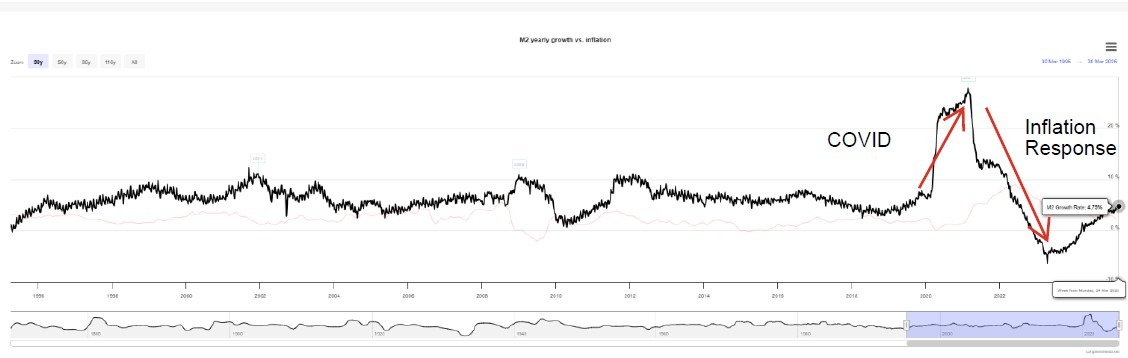

One thing that points to a positive in the economy is M2.

If you remember during COVID the FED blew out M2 (money supply) and caused inflation. You see that in the chart above. Today, M2 is growing at 4.29%, which is below the 6% level that many believe is needed for a healthy, growing economy. So, the FED has moved to a positive M2, but not what is believed to be healthy. Meanwhile, the economy tends to be slowing, largely because the FED had reduced M2 from the peaks of COVID to a negative level (basically soaking up excess money in the system). Recall what Milton Friedman said about inflation:

Part of the problem is that monetary policy works, but with variable lags. It’s part of the reason the FED tends to run the economy from one ditch to the other.

Finally, let’s get the news du jour, which is that we had “good” news regarding Chinese tariffs over the weekend.

Is this a real agreement or a framework? We will find out more in the not-too-distant future. But the markets like it. Mostly because tariffs have been ‘paused’ for 90 days, down to the base 10%. Furthermore, President Trump said:

So we will wait for that to come together over the next little while. Will this all help? Hopefully, but we have to see what the total results of all this are, not just with China, but all countries around the world. Remember, very little of the tariff news that has excited the markets, represents actual permanent changes. Markets have rallied on pauses, and the hard work of turning these pauses into enduring agreements remains.

If you have any questions or are losing any sleep, please reach out and we will be happy to have a conversation.