CPI numbers came out for January today and the market is throwing a tantrum. Why is that?

The Consumer Price Index (CPI) for the month of January came in at 0.3%, versus a 0.2% expectation. So, like a 2-year old, the market wants those FED rates cuts and wants them sooner rather than later. This inflation print calls into question whether they will get what they want. Let’s take a closer look at the CPI.

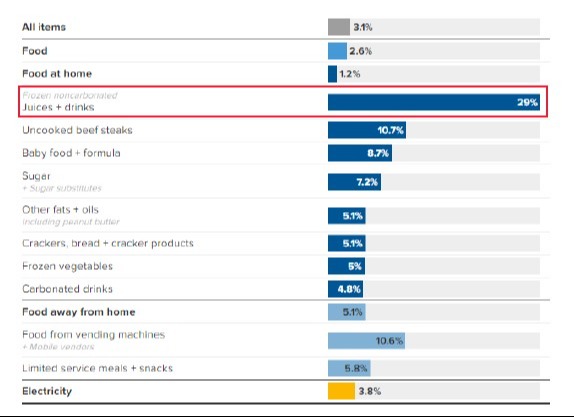

It appears that our good friends the Mortimer brothers are smiling, as their orange juice futures bets paid off in January. 😊

If anyone is a fan of Trading Places, you will know what I’m talking about.

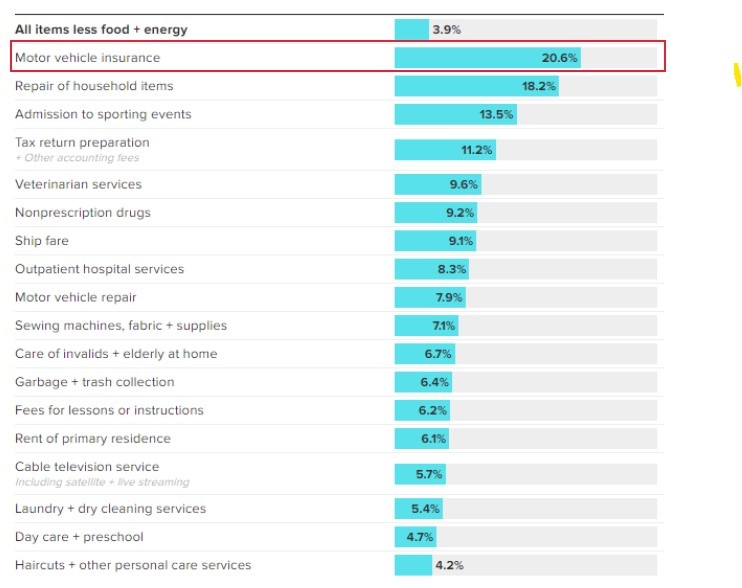

Also on the inflation front, not news to anyone who had to renew last month, car insurance was up considerably in January. They must have sampled my insurance renewal rates!

But on the good side, inflation over the last 12 months has decreased from 3.4% to 3.1%.

So, let’s talk about the four (really three possible outcomes).

- No Landing (not really an outcome)

- Soft Landing (minor recession and minimal job losses)

- Hard Landing (real recession and very noticeable unemployment increases)

- Hard Landing and something breaks (looks a lot like 2008)

Many “economists” have been calling for a ‘no landing’ scenario. Let’s take a quick look at what that means. But first, I have to give you an economist joke (sorry for any economists in the house!)

Anyhow, a ‘no landing’ scenario means the economy doesn’t slow down and therefore there is no reason for the FED to cut rates. FED chair Powell has said many times that they are looking for a slowdown in the economy. That should manifest itself in a higher unemployment rate. But, so far, we are not getting that.

It’s not to say a case can’t be made for lower interest rates, but if they lowered rates, wouldn’t that just increase all the activity that we are already seeing, thus making inflationary pressures greater? I think the answer is yes!

So, the market had expected the FED to cut rates in March, but now it’s moved that expectation to the May meeting. After today, it’s looking more likely that they don’t cut rates until July. As a result, the market freaks out and reprices the cut further out and we go on with life.

A ‘soft landing’ would likely produce some level of lower activity and therefore lower employment and lower inflation. This, of course, is the dream scenario.

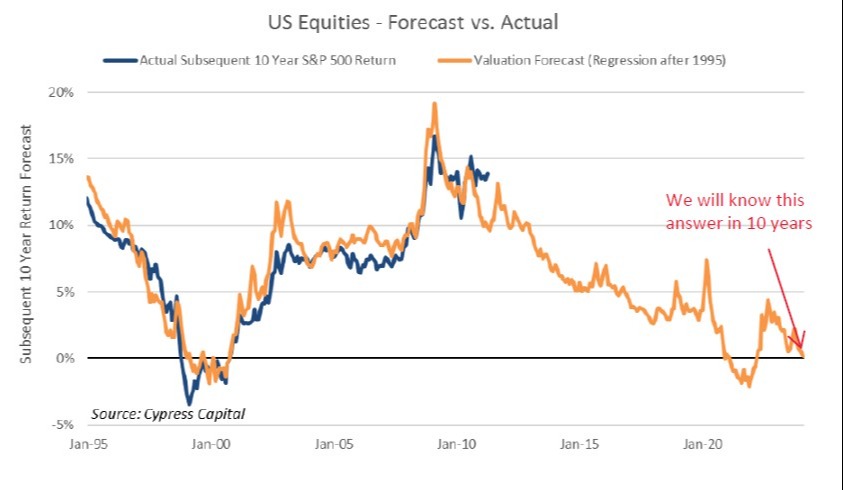

We’ve said for a long time that a soft landing was priced in, with a downside target on the S&P 500 of around 3600. Unfortunately, it looks like the market has gotten ahead of itself, as it was already pricing in those cuts and a soft landing. In fact, based on valuations, the market is expected to produce very little in real returns over the next 10 years.

That chart is not to scare you. It doesn’t mean there are no places to make money over the next 10 years. It just means that the market cap weighted S&P 500 (driven by the Magnificent 7 or 8) will likely tread water. If we are correct, we will see other parts do much better – like small caps, value stocks, and even bonds now that rates are much higher than they were several years ago.

The next two scenarios differ by how much “bad things” happen. I always like this quote from Chuck Yeager.

That’s the difference between a ‘hard landing’ and a ‘hard landing and something breaks.’ You’re not flying the plane tomorrow when something breaks.

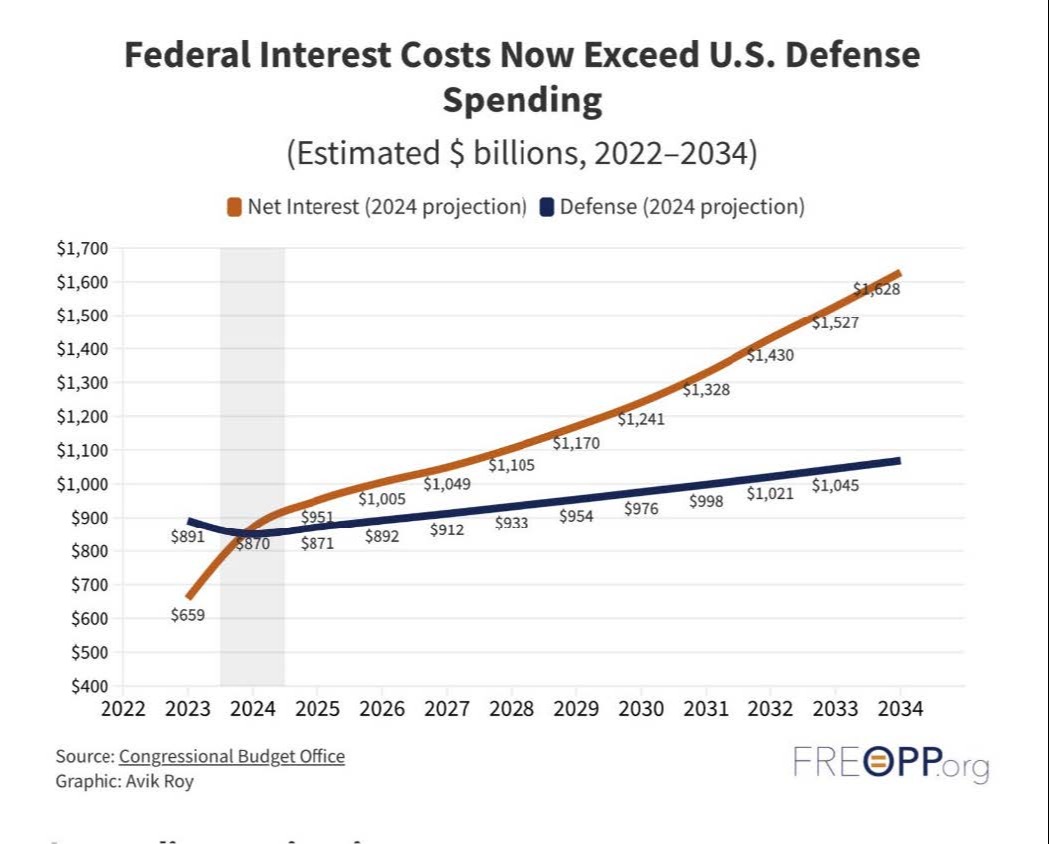

Unfortunately, we also can’t really tell what’s going on under the surface of the economy and markets. Debt is a problem at all levels now – consumers, businesses and government. We said a long time ago that during the Tech crash, much of the consumer and business debt was transferred to the banks. Then in the Financial Crisis, the bank debt was transferred to Governments (pretty much all governments). The big question is, when the governments feel the weight of trillions of (dollars, Yen, Euro, Pounds), what’s the answer?

For some the answer is just print more money. I think we have discredited that, but I also expect that central banks will try to take one more shot at “fixing” debt with money printing. In the US, debt will go from $34 trillion to $50 trillion (or higher). Yes, it may be true that the government never has to pay off the debt, but it does have to pay the interest. In fact, the Congressional Budget Office (CBO) just revised their estimates of interest payments. Last year the CBO expected interest payments on the national debt to be more than the defense budget in 2028. One short year later, look at what they came up with..

Yep, that’s right, 2024! Hey, they only missed it by four years. What was that joke about economists?

Let’s try to wrap this up. A ‘no landing’ is just higher interest rates and higher inflation until either the economy finally cracks, which would take us to some other scenario, or the FED resets what they view as acceptable inflation (meaning they move their inflation target from 2% to 3% or so). Many of you know that I have been saying that for a long time. The inflation rate going back to the 1930s has been about 3.15%. What makes this time any different than the last 90 years?

A ‘soft landing’ is like trying to thread a needle through a pin. It’s doable, but pretty difficult. And unlike an innocuous piece of thread, it’s hard to just “try again” with the economy.

The ‘hard landing’ (without so much economic damage) is what the FED wants. Of course, that would be the ‘soft landing’ scenario. Don’t let them fool you.

A hard landing with something breaking can’t be ruled out. In both hard landing cases, bonds will perform very well, as will all interest rate sensitive investments, as the FED will have to cut rates significantly.

That’s it for today, I hope you have a great week. If you have any comments or questions, please feel free to reach out to us.