As we are close to a correction in the stock market, it’s important to discuss where we are at and where we are going.

Last week we talked about the Atlanta FED updating their GDPNow forecast, and it said we were in the beginnings of a “recession” or at least a one quarter recession. We talked about how that may not be entirely correct, at least just yet, but why it happened and what the future of GDP is.

Let’s take a look at the market today (writing this on Monday).

If you look closely at the chart above, you can see that much of the RED is centered around the “MAG 7” and technology. Who’s in the MAG 7? Microsoft, Apple, Google, Facebook, Nvidia, Amazon and Tesla (you can add Eli Lilly if you want to make it 8).

Much of the rest of the market is either green or not very red.

If we look at the Magnificent 7 (or 8, depending on how you look at it), the S&P 500 is down about 4.5% for the year, while the Mag 7 is down almost 15%.

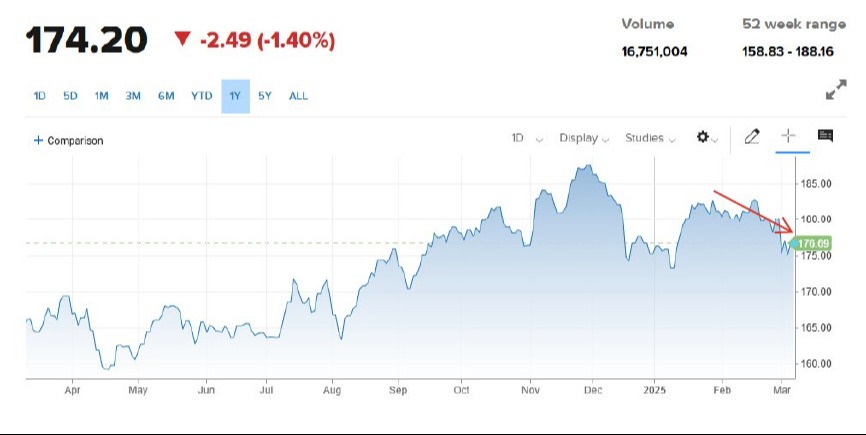

Meanwhile, our favorite S&P 500 indicator (RSP) is down less than 1% for the year. Here’s a look at the chart for that.

Not too bad.

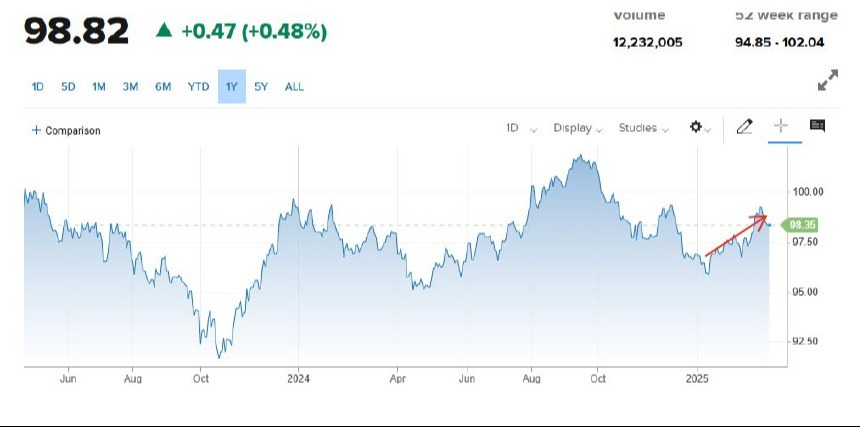

And if we look at bonds, they are actually up for the year. Here’s a look at the chart for the most commonly used bond index (AGG).

So why am I bringing this up?

Two reasons. One is to review the nature and frequency of corrections, and the other is to discuss diversification and portfolio management.

The first one is relatively easy. We should expect the following pullbacks/corrections/bear markets:

- 5%-10% pullbacks – about 2 or 3 per year

- 10% - 15% corrections – once or twice a year

- 20%+ corrections should happen every 2 or 3 years (called a bear market)

- 30%-40% corrections should happen about every 15+ years (or unless the Fed or government breaks something)

My point on this is we should see a few pullbacks in the markets per year. Is this going to be a “bear market?” Nobody knows for sure. Like we’ve said in the past, every 20% bear market starts with a 5% pullback, but not every 5% pullback ends in a 20% bear market.

This is also where we get questions about going all to cash. We can certainly go all cash with a few clicks of a button (that’s the easy part), but then we also have to know when the correct time is to get “back in the market.” That is a timing game, and we don’t think anybody is very good at it. What works much better in our opinion is to adjust the risk level of the portfolio via adjustments to the allocation, while always keeping an eye toward the long-term and the needs of your financial plan (more on this below).

We went to a “risk off” posture in our portfolios back in late-November – long before all this stuff happened and long before any of us were scared of the headlines. It looked a bit foolish for a few weeks, before it looked wise. At some point, we’ll go back to “risk on,” but only when the data indicates its appropriate. We might be early there too, but we’ll be following a process rather than emotion.

Now to discussing portfolio management. Depending on how much risk you are willing to take (your “risk tolerance”) and what your time horizon is (part of your “risk capacity”) will dictate how much stock (equity) we put in the portfolio. If you are young and have a long-time horizon, then perhaps a lot of stock might be appropriate. On the other hand, if you are planning on using the money in a year or two, perhaps it doesn’t make sense to allocate a lot to equities (if any). This can apply even if you are young – such as if you’re targeting a down payment on your first home!

That’s one part of portfolio management. The other part, in our opinion, is to look at factors in the market that are either conducive to taking risk or not. That’s the secret sauce.

We’ve said this before, many in our industry have a set it and forget it belief. We don’t subscribe to that thinking. Maybe we’re wrong, or maybe we are on to something. You see, when things are going along fine, rarely does someone have a worry about the market (or their portfolio). It’s only when things go haywire that human behavior comes into effect.

Never does it happen that the wheels fall off the proverbial bus when things are ok. It’s when we get bumps in the road that we, as investors, get nervous. When those nerves kick-in is when we start to question our process and our portfolio, and that is when we make mistakes. Don’t get me wrong, I get concerned just like anyone else. But it’s the process of setting up a portfolio and checking against our other indicators that gives me relative peace of mind.

But as long as things haven’t changed in my life, I shouldn’t change my portfolio (outside of what the model already does). Now, if I lose sleep over my portfolio, maybe I need to look at how much risk I’m taking. But moving to cash isn’t the way to go (in my opinion), because you have to be right on both sides of this coin – going to cash and putting that cash back to work. I haven’t seen anybody do it very well. I’m open to a better mouse trap, but what we’ve tried to create over the years, include some substantive changes a couple of years ago, is the best mouse trap I’ve been able to find.

That’s it for this week. If you have any questions or are losing any sleep, please reach out and we will be happy to have a conversation.