If you are like many, you have flocked towards the ~5% yields being offered by money market funds, CDs, and other “high-yield” savings accounts. Certainly a wise decision for those that need the stability that these types of accounts provide while also desiring to earn a little bit on their money. When bank savings accounts are offering 0.01% (or thereabout), a 5% yield in money markets provides a 500x return with no meaningful change in risk and the same level of liquidity. As the CapitalOne commercials say, it’s the “biggest no brainer in the history of” saving.

That said, all good things do eventually come to an end, and while we don’t foresee money market yields and CD rates dropping back to near 0% anytime soon, it is very likely that these rates will start to decline by year-end. Why so? Because they are driven almost entirely by the Fed Funds Rate, the overnight lending rate set by the Federal Reserve. Market participants are betting as if a September rate cut of 0.25% is basically a done deal, with the potential for additional cuts in the months to follow, as Chris showed in his weekly blog on July 16, 2024.

While a simple 25bps (0.25%) cut doesn’t meaningfully change the equation, it has got many clients and market participants wondering whether it is time to start moving away from cash. If so, what are the options?

UNDERSTAND YOUR LIQUIDITY NEEDS

First, your decision to have money parked in cash has to primarily be borne out of your financial plan. Cash holdings should primarily be for near-term needs, typically those expected in the next 0-12 months, sometimes up to 24 months (especially when yields are strong). If your looming cash needs haven’t changed, then your positioning probably shouldn’t either, regardless of how dramatically yields drop.

If, however, your timeline is longer and/or you were holding cash more so as a tactical investment decision, then a change in rates may prompt you to consider repositioning these funds into assets more suitable to your long-term needs. Let’s look at a couple of options that investors may consider (alone or in concert with one another).

LOCK IN LONG-TERM BOND YIELDS

You may have already read about or heard us talk about “locking in long term yields” currently offered in longer-term bonds. For some time now, with the yield curve inverted, you have actually been paid more to sit in cash (lower risk) than you could earn from long-term bonds (higher risk). This is counterintuitive, and yet has held true for many months now. Chris has talked often about the inverted yield curve, so I won’t go too deep into it here. In short, in a “normal” environment, the yield curve should be upward sloping, representing yields on long-duration bonds are higher than those on short-duration bonds and cash-like instruments. This makes sense, as you should be compensated for taking on additional risk. However, in some economic environments (typically when trouble is on the horizon), the yield curve will invert – and it clearly can stay there for quite some time. This distortion has likewise caused a distortion in how “safe money” has been invested. As the yield curve starts to normalize, it may necessitate a shift in how this same money is allocated.

One very important thing to understand is that as the Fed Funds Rate declines, it does not necessarily mean that longer-duration yields will drop as well. The Fed only controls the former, while the latter are controlled by market forces and represent the views of the millions of investors that make up the market on a daily basis. By investing in longer-duration bonds now, you can potentially experience one (or eventually both) of the following benefits:

- If long-term bond rates do not change, you continue to enjoy yields at or about their current levels. For example, the JP Morgan Core Bond Fund (WOBDX) currently yields ~4.5%. If the Fed cuts rates by 1% but long-term rates don’t budge, you’ll be in a position where the yield on this fund exceeds what you can get from money markets or the like. Remember, the yield on a 30-yr bond is fixed for 30 years. The yield on money markets changes daily.

- If long-term bond rates drop, the price of the bonds you already own will climb, and this climb could potentially be quite significant. Let’s say you have $100,000 of that aforementioned JP Morgan Core Bond Fund. If interest rates dropped 1%, those bonds should now be worth ~$106,100…while you continue to enjoy that ~4.5% yield for some time, bringing your total return for the year to ~10%. Recall, as interest rates drop, bond prices climb, and as interest rates climb, bond prices fall (as we saw in 2022).

Note that this is not a risk-free proposition. Notice that these two bullet points talked about rates staying level or dropping. But as noted, if rates climb, bond prices drop (a risk). While the odds of such a move are currently low in the near-term, you cannot eliminate this risk from your calculus. That is why your financial plan and the timelines it affords are so crucial to understand.

We should also mention that you do not have to proceed all the way out on the curve directly to long-term bonds. While these do present a potentially valuable opportunity currently, you can also consider “short duration” bonds, which act a bit more like cash, but with some potential for upside as rates drop.

INVEST IN EQUITIES

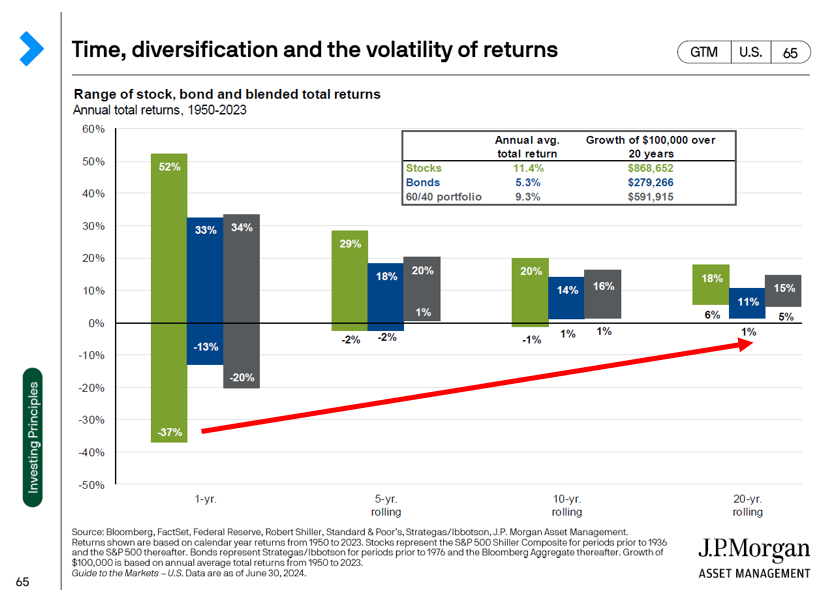

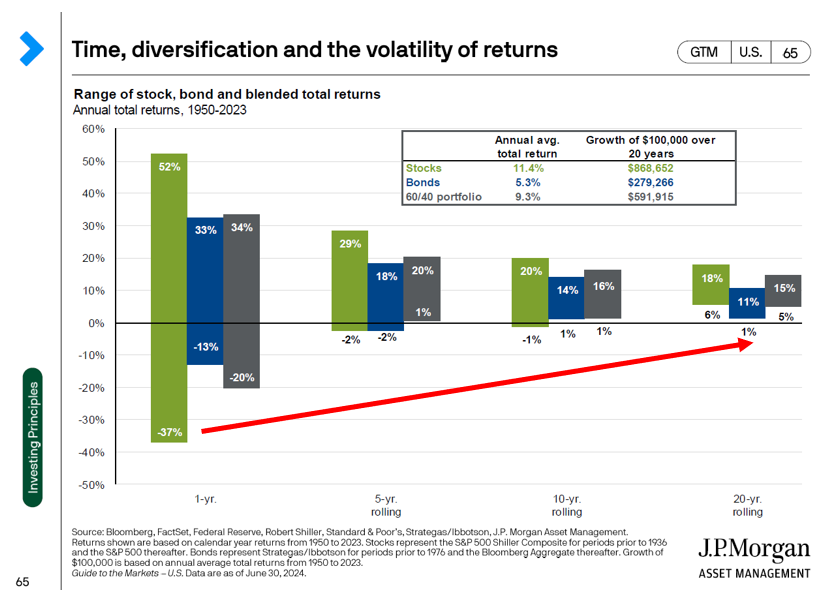

If you have been holding cash simply as a hedge against volatility and don’t actually have liquidity needs in the near future, you may want to consider investing that cash in equities. This generally represents one step further out on the risk spectrum than long-term bonds, but also brings with it a greater potential return in most circumstances. The following chart, which I utilize often, illustrates both this point and the fact that long term investors are generally well-served by taking risk.

The math behind investing in equities over the past two years has been greatly impacted by the concurrent steep climb in the Fed Funds Rate, as that “risk-free rate” impacts what is called the “net present value (NPV)” of future cash flows provided by equities. The higher the risk-free rate, the less valuable future cash flows become, which typically drives down equity prices. This particularly hits hard at “growth” companies where the majority of future cash flows are projected to come long in the future. On the flip side, as this risk-free rate drops, the value of those future-dated cash flows increases, sometimes quite substantially, bringing the value proposition of equities further into focus. So, as we see the Fed Funds Rate start to drop, we should see a concurrent increase in equity prices, in most circumstances. The risk here is that a current cash-heavy investor may miss quite a bit of upside while waiting to make the move out of cash.

LET'S WRAP IT UP!

This is not to say that you should make a wholesale, overnight decision to throw caution to the wind and shift all of your cash into riskier assets. However, it is an invitation to consider the “risk” of continuing to hold cash as yields drop. Does a substantial cash position still fit with your financial plan? Do you have too much or too little given your current and expected circumstances? Will the safety and comfort that such positioning offers actually prove detrimental to your financial plan, introducing a hidden risk via what is otherwise called a “risk-free” asset? These are questions that every investor needs to be asking. No, we’re not heading back to 0% rates anytime soon, in our opinion. But just as the dynamics changed as we moved out of that reality, the dynamics will again change as we (potentially) move off of a generationally tight monetary policy.