Oh good – here we go again talking about what happens when you die! I promise it’s not all we think about around here (remember, we also talk about interest rates and inflation!), but we’d be remiss to not give it some thought from time to time. After all, you can’t change things once it happens – so getting things correct right now is imperative. In today’s edition of “things to do before you die (but not the day before),” we’re going to look at beneficiary designations. Why are they important? When should you review them? How do you update them?

Like most topics, there are a number of complexities around what seems like a relatively simple topic. We’re going to cover the key areas that impact 99% of you, and hopefully distill it all down so that it’s easily understood and acted upon.

Let’s start with the basic questions of “What is a beneficiary designation, and doesn’t my Will take care of that?” A beneficiary designation is something you place on an account that specifies who receives the assets from the account upon your death. In most cases, this applies to retirement accounts and health savings accounts, though taxable brokerage accounts also have a form of beneficiary designations called “TOD” (Transfer on Death). Yes, your Will also does the job of directing your assets upon death – but beneficiary designations have an added feature that make them particularly powerful and attractive – they allow these assets to avoid probate.

By becoming non-probate assets, these accounts more quickly pass to your designated heirs without the delays, costs, and headaches of the probate process. Any assets not covered by a beneficiary designation do still remain subject to probate, unless they are in the name of a Trust, as detailed in a piece we sent out in August 2021 (access here).

Another very important note is that beneficiary designations take precedence over anything declared in your Will or Trust. In an extreme example, let’s say you named your boyfriend the beneficiary of your IRA, but then broke things off and married someone else years later. When you got married, you went and paid a couple grand to an attorney to draft up some nifty estate docs, declaring that your spouse receives everything when you die, but you forgot to update the beneficiary on that old IRA. A year later, you pass away. What happens? Your spouse gets everything – except that old IRA. In fact, your ex-boyfriend will get his hands on that account likely before your husband ever gets possession of everything left to him, as he’ll still be sorting through probate as that ex cashes in the IRA for a long-awaited overseas vacation.

Now that we’ve got your attention with extreme (but albeit real life and very plausible) example, let’s consider a few more things about this important topic:

#1 - How often should you update your beneficiaries? It’s unlikely that you need to update them very often, but they should be reviewed at least annually. Reality is that circumstances change. Relationships evolve, people pass away, your estate plan changes, and estate and tax laws change. Any of these can be reason to need to change your beneficiaries.

#2 - How do you review your beneficiaries? Give us a call and we’ll be happy to walk you through who’s currently listed. Likewise, you can see this information at Fidelity or wherever your account is held.

#3 - Who can be named as a beneficiary? Candidly, just about anyone! You can name any individual (including minors), charities, estates, or Trusts – or any combination of the above. Naming your estate is typically not advisable, as that would simply put the assets into probate (one thing we were trying to avoid) and has severe negative tax consequences for your heirs. Likewise, naming a Trust is often not advised under current estate and tax law, as doing so can have significant negative tax repercussions in many cases.

It's important to note that on a “qualified retirement plan” that is governed by ERISA (e.g. 401(k)), your spouse must be the sole beneficiary unless he/she provides consent. You can then name anyone as a contingent beneficiary in case your spouse predeceases you.

#4 - Tell me more about contingent beneficiaries! These are persons, charities, or trusts that you name to receive the proceeds from your account in the case that your primary beneficiary predeceases you and you fail to update your beneficiaries between the death of your primary beneficiary and your own passing. Nothing more to it than that.

#5 - What does “per stirpes” mean, and what about “per capita”? When you complete a beneficiary designation, you will normally be prompted to choose whether the assets pass “per stirpes.” What does this funny phrase mean? It is a Latin phrase that translates literally to “by roots” or “by branch.” The other option (which is typically the default) is “per capita.” How do these compare? Bear with me here, as this illustration is a bit long, but I think it’s pretty clear and helpful.

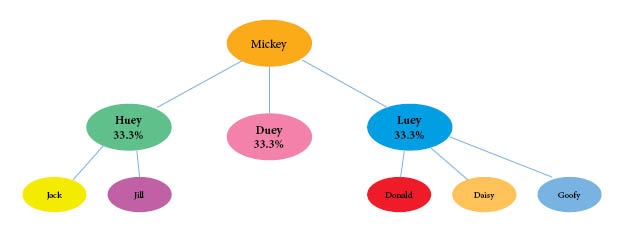

Let’s start by assuming you are named Mickey and you were married to the lovely Minnie, who passed away three years ago. Together you had three children and five grandchildren. Since Minnie predeceased you, you desire to leave 100% of your retirement account in equal shares to your three kids (Huey, Duey, and Luey). In that case, your beneficiary designation would look like this:

Your three children would then be able to designate their inherited account to whomever they choose, subject to aforementioned spousal restrictions when applicable.

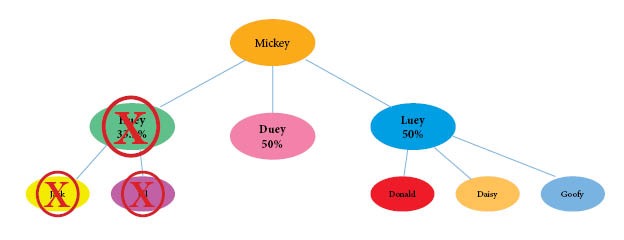

Now let’s assume tragedy hits and Huey passes away before you do. Here we’ll be able to illustrate the difference between “per capita” and “per stirpes.” With per capita, Huey is simply removed from the equation, and the percentages left to his siblings change to 50%/50%. Even if Mickey wanted Jack and Jill, two of his beloved grandchildren, to receive something, they would not (unless he updated his beneficiary designations after Huey’s passing). Here is what this all looks like, using our same Easter egg chart from above:

Now, let’s assume instead that Mickey had checked the “per stirpes” box when he completed that beneficiary form years ago. In this case, Duey and Luey would still receive their original share, while Huey’s children would receive his share of the account, split equally. Here’s what this looks like:

As you might imagine, these illustrations could quickly get quite complex, depending on the number of beneficiaries, children, grandchildren, etc. involved. Regardless, I think these illustrations illuminate the key points and should serve as a good primer for you as you think about your own beneficiary designations in consultation with us and your estate attorney.

#6 - Do the same rules apply to Health Savings Accounts? Yes and no. The same beneficiary designation rules do apply with HSA accounts. However, tax treatment of inherited HSA assets is dramatically different than with retirement accounts, so you should carefully consider who you designate these assets to. The differences in these rules is beyond the scope of this briefing, but we’re happy to field your questions on this if you are interested.

#7 - What about non-retirement accounts? We mentioned earlier that you can use “Transfer on Death” designations with some non-retirement accounts in order to avoid probate. You can also use certain joint ownership designations (e.g. Joint With Rights of Survivorship) to achieve the same purpose. Proper use of these designations will depend heavily on the structure of your estate plan, so please consult with us and your attorney prior to making any changes with these accounts.

#8 - Last question – how do I make an update? If this piece has prompted you to want/need to make an update to your beneficiary designations, the practical question that follows is, “How?” And it wouldn’t be a planning briefing without saying “it depends!” In general, though, the process is quite simple. If your account is with us (e.g. IRA), you need to complete a Fidelity Beneficiary Form. You can list your beneficiaries directly on that form, or you can note that you are supplying “Special Instructions” as provided by your attorney as part of your complete estate plan. If your account is with your employer (e.g. 401(k)), you should contact your HR department for instructions. Sometimes the designations are kept on file at your company, while other times they are maintained by the Plan’s recordkeeper. We will be happy to work with you on this, regardless of where the account is housed.

That should about wrap things up. As always, we welcome your questions – whether they are about this or about anything else that may have come to mind as you muddled through 3+ pages of discussion on such a topic as this.