For the last several months, the market has been worrying about an economy that is too hot and that maybe inflation is coming back.

Aside from some residual sticky inflation, I think our belief is that inflation is not meaningfully going to spike in the near future. By spike, I’m thinking numbers that would cause the Federal Reserve to start tightening again.

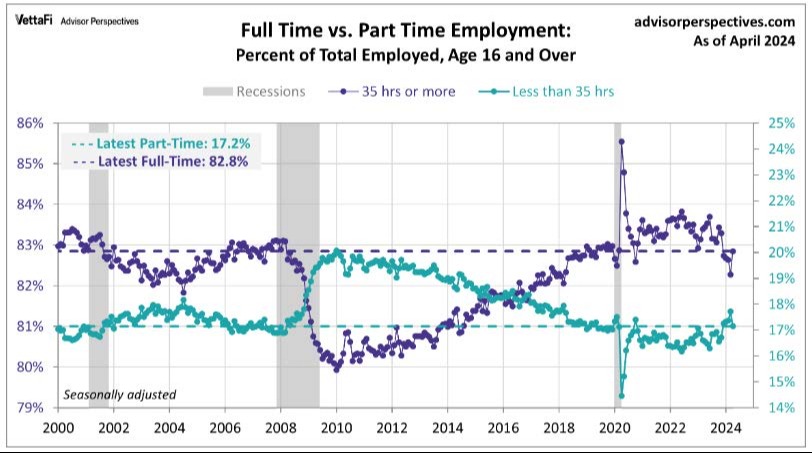

In fact, we’ve been more arguing that things are not as “good” as they look on the surface. Yes, the jobs data has been stronger than expected, but full-time jobs have seen a reduction over the last year, while part-time jobs have seen an increase.

And the way that the labor department calculates new jobs is by the actual job. So, if someone has three part-time jobs, that is considered three new jobs. Even if it is only the equivalent of a full-time job. Anecdotally, Andrew mentioned the other day an acquaintance who had lost his job, and his wife had picked up two additional part-time jobs as a result. Do you think the family is better off in this circumstance? The simple math of the employment numbers would say yes. Reality would say otherwise.

Meanwhile, the initial non-farm payroll numbers have been overstated and have subsequently been reduced over time. I’ve mentioned this before, but David Rosenberg of Rosenberg Research Associates has calculated that jobs were overstated by 443,000 in 2023.

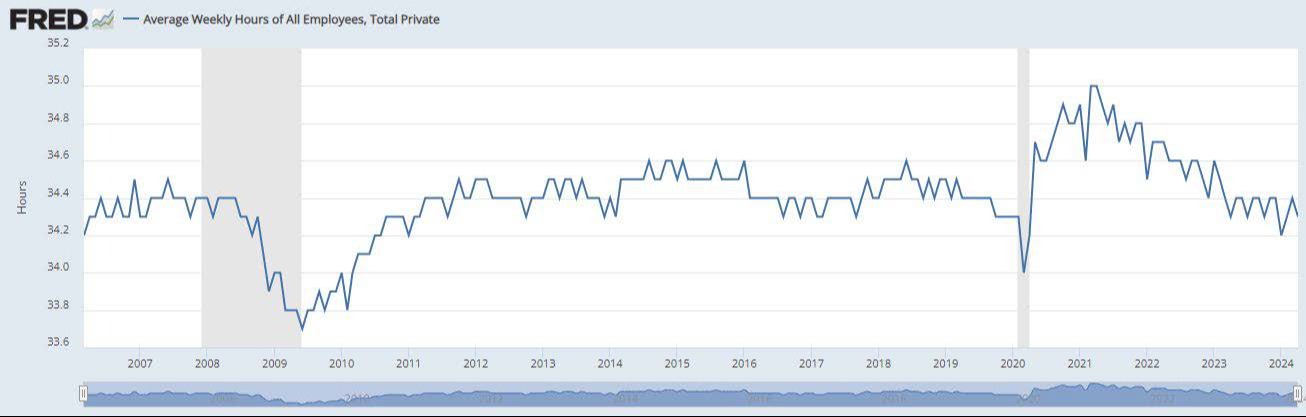

And that’s not all. The hours worked have come down tremendously over the last few years. See the chart below.

You can see that total hours worked peaked at 35 hours per week and now are at 34.3 hours per week. That may not seem like a lot, but that is 2% less per week that people aren’t getting paid. Over the course of a year, that’s the equivalent of one full 35-hour work week.

So far, we have overstated jobs numbers and a work week that has been shrinking. Those two things are not inflationary, for sure.

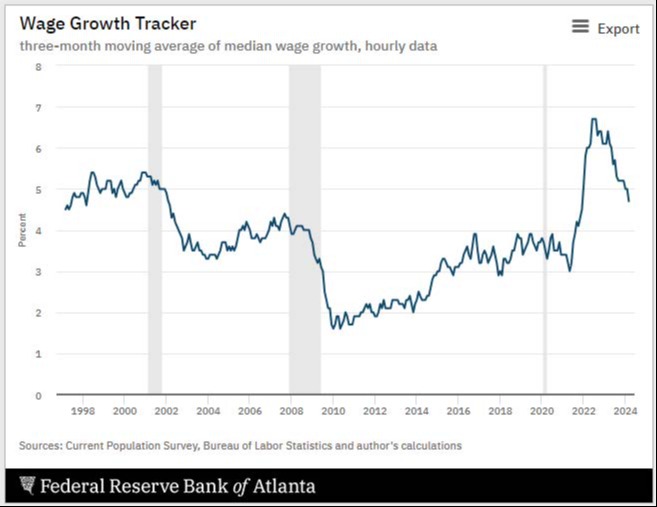

On the flip side, we have wages that are quickly coming down into the range they were pre-COVID.

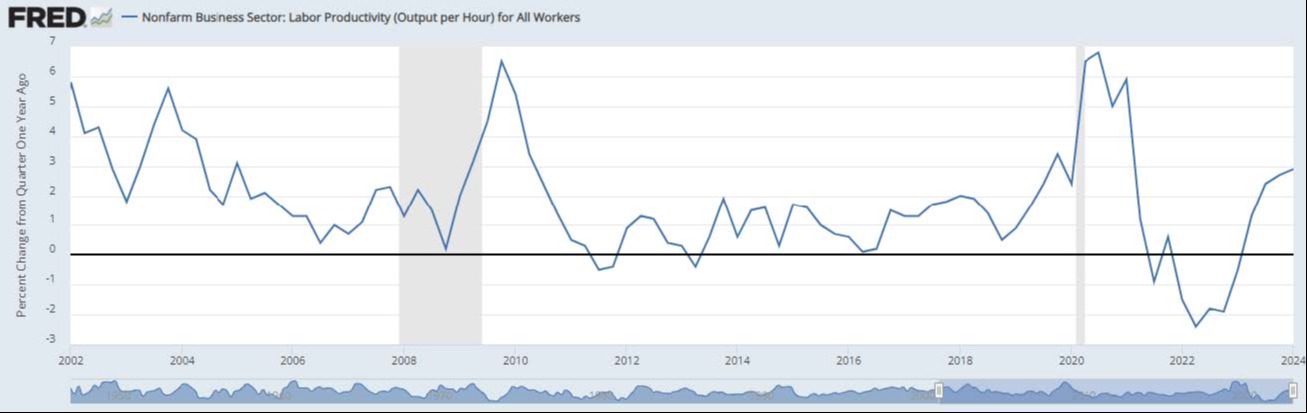

And in turn, productivity is increasing.

So, let’s put this all together.

- Softer jobs numbers after revision

- Less hours worked per week

- Wage inflation coming back down to historical norms

- Productivity increasing

All these are, if not deflationary, at least not inflationary. And then came last Friday.

Sorry for the small font. Here’s what the numbers said. New jobs were only up 175,000 versus an expected 240,000. The unemployment rate went up to 3.9% from 3.8% while hourly wages went up only 0.2% for April versus an expected 0.3%. On top of that, the ISM services index showed 49.4 (remember below 50 represents contraction).

Now, to be clear, I’m not saying the coast is clear because of one set of numbers. What I am saying is that April’s numbers support our case that the economy is actually slowing a bit to a level that the Federal Reserve can be comfortable cutting rates (or at least for sure not raising them).

Remember, we can (and should have) rising wages, but those wages don’t have to be inflationary if the corresponding productivity keeps up with wages. And we think they are and will continue to. Technology is a huge deflationary tool and AI will be likely a greater source of deflation in the decades to come.

In light of the market realizing that the FED may actually have room to cut rates, the dismal month of April has so far turned into a very nice first week of May. The model continues to add to its bullish stance, which says to expect a broadening out of the market and an outperformance of companies other than the Magnificent 7 (or 8).

Speaking of those Magnificent 7 or 8, the only one that hasn’t reported Q1 earnings yet is Nvidia. That will happen later this month. So, of those 6 or 7 companies that have reported, the only real stinker was Meta (Facebook). Every other company beat earnings and stockholders have been rewarded accordingly. It’s also part of the reason the market has rebounded in the first week of May.

If we are correct and the economy cools to a sustainable level and corporate earnings grow like they should, that should be a nice tailwind for the markets. The old adage, ‘sell in May and go away’ may not be a very smart thing to do this year. Add to that the possibility one or two interest rates cuts from the FED, which also would be helpful for profits and business in general.

That’s it for this week, I hope you have a good week. Reach out with questions or comments