So much has changed in the last two weeks! Fall is officially here, kids are back in school, the Mariners are on the outside looking in on the playoffs (ok, that hasn’t changed), and college football (or should I say NFL minor leagues) has started.

And how about a big cheer for the Cougs (and the PAC12) beating the Huskies in the BIG10! Not that I care that much, but I’m still sort of bitter about college football turning into a money grab. Not that it’s different now than the last 10 years, but abandoning your conference for the sake of money leaves a bad taste in my mouth. Enough of that for now!

In my last post, I discussed the FED meeting and how the market was mostly pricing in a 0.25% rate cut. Well, that changed really quickly when word started to get out that the FED was considering a 0.5% cut instead. And that’s what we got last Wednesday.

The other thing I talked about was the tone from Jerome Powell in his press conference. I would say he generally hit the notes that I thought he should. And the market has responded pretty well since then. But that sort of begs the question. Why the big cut, and does that mean they are concerned about the economy?

First off, if we consider they could have cut by 0.25% in July, then followed with another 0.25% last week, they would be in the same place, and nobody would even question their motives or concerns. Though inflation is not down to their targeted 2% level, it is getting toward that point. Just like an airplane landing, you need to transition to your landing before you touchdown. If you don’t, you end up crashing into the ground. It’s called ‘flaring.’ I’d say that’s what the FED is doing right now, flaring for landing.

As we know, the other part of their dual mandate is full employment. So, crashing the economy just to get inflation down doesn’t serve their full employment mandate. The flare accomplishes both, by slowing the economy down, while not crashing employment. Remember, full employment doesn’t have to cause inflation.

‘Inflation is too much money chasing too few goods.’

The inflation we had was caused from the government putting $7 trillion of new money into the system, much of it while most businesses were closed or under reduced production. This is the classic definition of inflationary conditions.

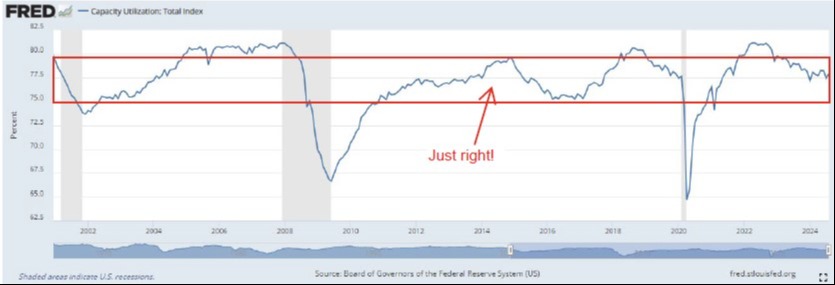

Today, most businesses are running at full capacity. Take a look at the capacity utilization chart below.

You can see it is back in that 75%-80% range it’s been in for the last 20+ years. With that, the big question still remaining is whether the economy will tip into recession?

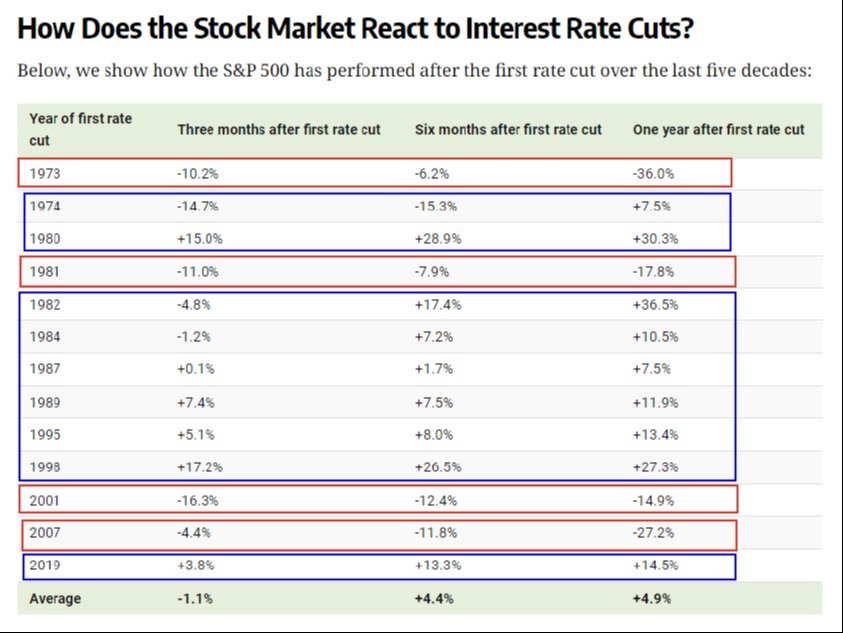

If it does, I think it will be a very minor recession (we could call that a soft landing). For most people it probably won’t feel like a recession, and the market may not even react as if it’s in a recession. In fact, here is what the market has looked like over the last five decades when the FED starts cutting interest rates. Courtesy of our friends at Visual Capital.

You can see that the market is generally positive over 6-month and 12-month time periods. Where the market wasn’t positive, was when we were in a “real” recession (a hard landing). 1973, 1981, 2001 and 2007, most notably. Are we in that type of period now? NO. Could we be? YES, easily.

But either the FED would have to make a mistake (I think they are doing things right so far) or something else in the economy would have to break. Could something break? SURE. But right now, we aren’t seeing things that would throw up major red flags. Don’t get me wrong, I can come up with reasons the world is going to fall apart. War in Europe and the Middle East, massive government debt, and consumer credit card debt come to mind, and I could easily list 10 more.

Of all those, the wars are the things that could spin out of control. We’ve talked about this before. That would only be a problem if NATO and China/Russia got into direct conflict. So far, those parties have mostly stayed on the sidelines. Government debt will be a problem in the future. I don’t think that day is here yet…

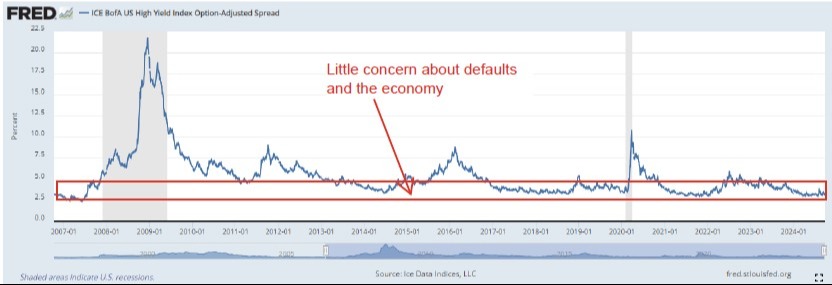

Here is a chart that we regularly look at to see risk building in the system. It is the high-yield spread over treasuries. When the spreads are tight, the market is not really concerned about much. Today, it looks very normal.

Finally, don’t get confused when you see a news story about how lower interest rates (from the FED) will result in lower interest rates on mortgages, autos, and credit cards. Yes, there is some benefit, but the FED doesn’t control long-term interest rates. It has some influence on short-term rates, but don’t expect relief unless you have loans tied to FED funds, PRIME or SOFR. If you do, you will see near-immediate cuts in interest rates.

As far as mortgage rates are concerned, they have already come down. Unfortunately, those lower rates have not translated into higher home sales. Here’s a good article from CNN if you’re interested.

That’s it for this week. Enjoy your first week of Autumn. If you have questions, please reach out and we are happy to have a conversation. Perhaps the M’s will surprise us, and that conversation can include a talk about their odds in the playoffs!